Living Large on $30,000 A Year, Get Ahead on a $30,000 Budget

Over the last decade Mrs. C. and I have increased our earnings substantially. During our first five years together, from 2005 – 2009 we averaged $30,000 a year. During this time we had 1 kid the entire time, and our second kid was born towards the end of 2008. During these years we were able to buy a house and save up thousands of dollars. This wasn’t always easy and there were of course stressful times. Not only did we save money while making $30,000 a year, we learned how to save money making $30,000 which has allowed us to save much, much more as our income has increased. How did we make it on $30,000 a year? Check out our budget below:

Over the last decade Mrs. C. and I have increased our earnings substantially. During our first five years together, from 2005 – 2009 we averaged $30,000 a year. During this time we had 1 kid the entire time, and our second kid was born towards the end of 2008. During these years we were able to buy a house and save up thousands of dollars. This wasn’t always easy and there were of course stressful times. Not only did we save money while making $30,000 a year, we learned how to save money making $30,000 which has allowed us to save much, much more as our income has increased. How did we make it on $30,000 a year? Check out our budget below:

$30,000 A Year Breakdown; Our $30,000 Budget:

These numbers include my income, Mrs. C’s income, and any unemployment benefits. Yes a couple years are above $30,000 a year, but on average we are right there.

- 2005: $23,839

- 2006: $29,617

- 2007: $36,562

- 2008: $22,452

- 2009: $39,920

$30,000 a year is about what two people working full time at minimum wage jobs would earn in a year. During this time period Mrs. C. and I spent a good deal of time in minimum wage jobs. The bulk of my earnings for 2005 – 2007 was from working as a cook at KFC. Mrs. C.’s earnings were primarily from working in retail as a stocker at Meijer and as a parts salesperson at Autozone. I started working nuclear plant outages at my home plant in 2006 in addition to my KFC work. In 2008 we had a large dip in income because I only worked one outage, which lasted about 5 weeks and Mrs. C. was pregnant with our first child together and was on a reduced work schedule. We listened to the Dave Ramsey Show and bought the book The Total Money Makeover

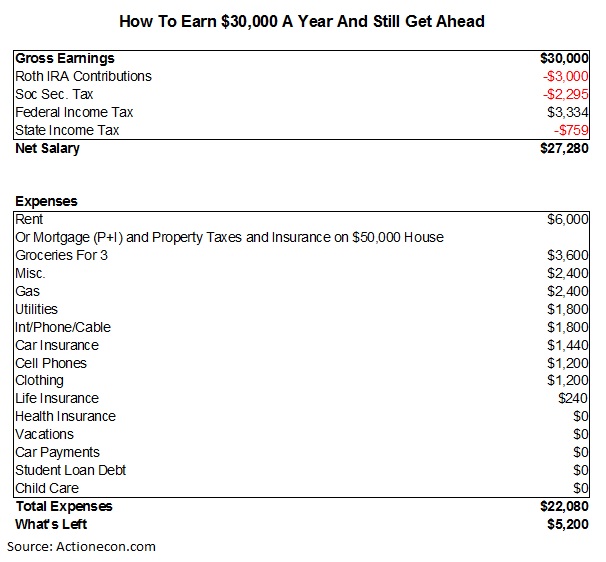

How To Earn $30,000 A Year And Still Get Ahead:

The Top Costs In Our $30,000 Budget:

Housing: By far the most expensive item is housing, taking up $6,000 a year. Where we lived in Benton Harbor, MI this was the cost to rent a 2 BR 1,000 square foot apartment in an apartment complex. When we bought our first home in 2006 the cost of the mortgage with taxes and insurance added in was just shy of $500 a month. We had purchased a house that cost just under $50,000 and had it on a 30 year mortgage. Our home value was less than twice our annual income. Saving money on housing, which is most Americans largest expense is the best place to start saving money, especially when earning $30,000 a year.

Groceries: Our Grocery budget was the second highest expense. At $100 per month per person we were doing pretty good. We are still at this level of spending today. We accomplish this by buying extra items when things are on sale and by rarely eating out.

Misc: The Misc. category is for things that come up unexpectedly. This is for things like car repairs, home maintenance, and dental work. Some months the total would be close to zero and some months it would be closer to $500, but it evened out to around $200 a month.

The Lowest Cost Items In Our $30,000 Budget:

Federal Income Taxes: When living on $30,000 a year or less, there are some tax advantages that are not available to higher income workers.

The Retirement Savers Tax Credit: The retirement savers tax credit is staggered based on income and can provide an up to 50% tax credit on up to $2,000 per person. This means in a two person household if each person saves $2,000 in their retirement account, then each person can get a tax credit of $1,000. This is huge! Unfortunately when Mrs. C. and I were earning in this range of income we were more focused on saving money for a down payment on our house and building an emergency fund that we weren’t even aware of this tax credit.

Since this is a non-refundable tax credit, it will only take the workers tax down to zero dollars. Because there is no tax liability a traditional IRA makes no sense, so we put the money in a Roth IRA. While Earning $30,000 a year in a family of 3 the Retirement savers tax credit can only provide a $525 tax credit, any contribution over $1,050 will not receive this credit. Due to this, I would put the extra retirement savings over 10% into a taxable account earmarked for retirement. For a single person or someone claiming head of household, it would make sense to put more of their savings into a retirement account to maximize this credit.

Child Tax Credit: The Child tax credit is a $1,000 tax credit that can be fully refunded under the Additional Child Tax Credit.

The Earned Income Tax Credit: This tax credit is for low income people, especially those with children. The Earned Income Tax Credit is fully refundable and can be up to $6,269 depending on income level and number of children in the house. Here is a chart showing some of these data points. In this situation with a $30,000 Gross Income and a married couple with 1 child, the Earned Income Credit would be $2,334.

Effectively, these tax credits increased Gross Income by over 10%, and allow for a much higher savings rate.

Health Insurance: When making $30,000 we didn’t have health insurance. Today, for a family of 3 $30,000 in earnings would put them at right around 150% of the Federal Poverty Level. In most states this would result in being able to acquire a bronze plan at no cost or a silver plan for around $100 per month with cost sharing benefits for the deductible, with the child being covered by medicaid.

Vacations: Vacations are optional and while earning $30,000 a year It doesn’t make sense. For recreation we would go to different local parks, the beach, and occasionally to our local zoo.

Car Payments: Car payments are a big ripoff and thankfully we only fell into that trap for a very brief period of time. Overtime we slowly moved up in cars, but for the most part have driven cars that cost well under 10% of our income level, and with one exception, have always paid cash.

Child Care: Mrs. C. and I mostly worked opposite shifts so that we would avoid paying for childcare. Occasionally my mother in law would watch our kid. Childcare is extremely expensive and it is far better to arrange your schedules in a 2 worker household to avoid paying childcare than it is to pay it, at least at this income level. For the most part childcare costs the same total dollar price regardless of whether you earn $30,000 a year, $50,000 a year, or $100,000 a year. Some states offer assistance with child care costs on a sliding scale based on income.

Saving Money on a $30,000 Budget:

I’m not going to lie to you, it certainly is not easy to save money making $30,000 a year, but it is possible. We rarely ate out or did anything recreational. We didn’t go watch movies in the theater or go to theme parks or shows. We didn’t have cable or high speed internet for most of the time we were earning under $30,000 per year and we drove cars that were paid for, but certainly classified as beaters. Mrs C. went through probably 5 vehicles in this time frame ranging from a $300 Buick Regal all the way up to an $1,800 Plymouth Voyager. The strategy that worked the best for me to save money on a $30,000 budget was to classify ever single expense with a fine tooth comb as a need or as a want. We then paid only the need items and bought virtually nothing in the want column.

After developing a $1,000 emergency fund, it makes sense to set up a Roth IRA and begin retirement savings. I would recommend starting a Roth IRA at Betterment because with Betterment you can get started investing with as little as $10 and you can set up automatic payments so that you don’t have to think about your retirement contributions every month.

Where Could This $30,000 Budget Be Cut:

Increasing Your Income:

You can only cut a budget down so much. This budget is constructed at $22,000 of spending, which is extremely low. I personally believe it is possible to cut it down significantly, however the biggest gains possible will be from increases in income. The good news about living off of $30,000 a year is that increasing your income can be done much easier than at higher income levels. Working more hours, even at minimum wage can have a substantial impact on yearly gross income.

Dedicating a few extra hours per week towards finding a higher paying job is also a great investment in time. From my time working at KFC for three years I knew dozens of people who left a job earning around minimum wage to jobs earning $3 – $5 above minimum wage. This type of pay raise, implemented across two people could increase yearly earnings from around $30,000 a year to around $45,000 per year, which would be a MAJOR improvement.

During the time period we were earning around $30,000 a year I invested a lot of time into education. I attended community college, and the bulk of it was covered by a combination of scholarships and tax credits. My parents did pay for the rest of my college, which I am extremely thankful for. Using tax credits and scholarships I was able to get the true total cost of my 4 year degree down to $13,000 over an 8 year period of time. Beyond investing in college, there are other ways to invest your time to make yourself more marketable. I took the CAPM exam last year, which cost $300 and passing that test led me to a job opportunity that paid around $60,000 a year.

Housing: During several different periods in our lives we have rented out rooms to friends and family. If you can get over the added stress of having another person live in your home, you can save a lot of money on your budget. At an absolute minimum I would charge $250 for renting a room, plus the tenant has to cover his own groceries. This would result in a budget cut of $3,000 per year, dropping yearly expenses to $19,000.

Refinancing is another major source of saving money on a house. Refinancing to a shorter term mortgage will help you pay off the house quicker without having to take action every month and you may end up actually spending less per month on your house from saving money due to a lower interest rate. Check out the current interest rates for a refinance at LendingTree.com. When we bought our first home over 10 years ago our interest rate was 7.37%! When we refinanced 3 years ago we were able to drop the payments by $100 per month and shorten the term.

Groceries: The Grocery budget can be cut substantially through proper meal planning, buying in bulk and shopping at discount stores. Cutting out optional foods like pop and convenience foods like pre-made and processed chicken nuggets and peanut butter and jelly sandwiches is another easy cost reduction. It certainly would be possible with some concentrated effort to cut this grocery bill in half to $1,800 per year ($50 per person per week). This brings the yearly budget down to $17,200.

Gas: This budget has a lot of money allocated to gas. At the current price of $2 per gallon this budget has 100 gallons of gas built in, enough to travel 3,000 miles in a typical 4 cylinder car. With proper trip planning this could be cut down by at least a quarter. The bulk of these miles and trips to and from work on a daily basis. Cutting fuel costs by 25% would save $600 per year, dropping spending to $16,600.

Internet/Cable/Phone: All of these are optional, especially for people who have cell phones. Cutting Comcast out of your life is probably one of the most exhausted personal finance topics on the internet, so I won’t dwell on it. In this already low budget it is a spot to consider cutting, but in the grand scheme of things it is a small expense. Cutting Comcast will drop yearly expenses to just under $15,000.

At this point the costs have been cut down substantially, resulting in a savings rate of over 50% while earning $30,000 a year. It is important to keep spending in check, but as I mentioned above the biggest gains will be from increasing income and dedicating more time and effort towards that side of the equation.

Winning On A $30,000 Budget:

It is possible to live off of $30,000 a year and still get ahead; but you have to put in a lot of effort. If you are earning $30,000 a year strive to at least hit a 25% savings rate, and then focus on increasing your income. Challenge yourself to hit $50,000 over the next 12 months, Then read my article on How To Get Ahead Earning $50,000 A Year and set a new goal for $60,000 a year. Increasing your savings rate is the only way to build wealth and to build wealth quickly. Don’t allow yourself to fall into a self defeatist attitude that you can’t get ahead because you don’t earn enough money.

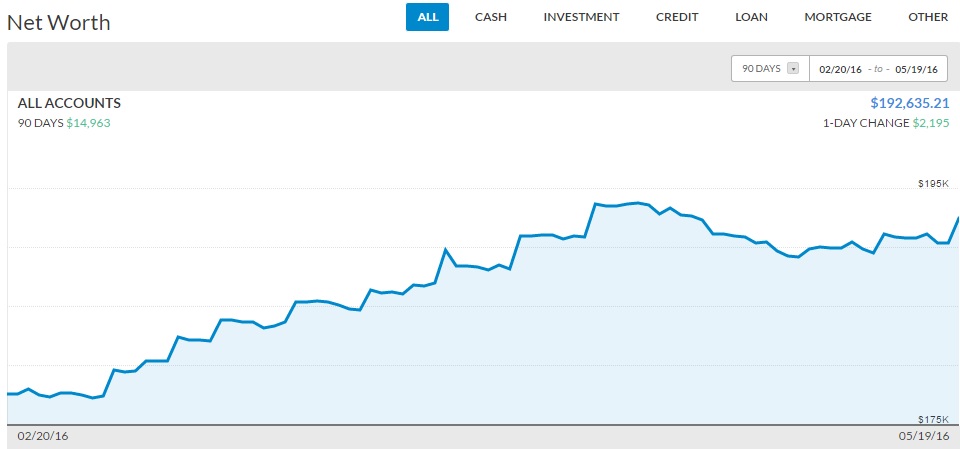

Our current goal is to reach financial independence in 16 short years. To stick to our goals and track all of these accounts I use Personal Capital. It’s a free app and makes keeping track of your progress a snap. We have multiple bank accounts and Personal Capital combines them all together to give a full picture of our cash flow. Currently you can get a free $20 Amazon gift card when you create a free Personal Capital account through this link and link an investment account. Here are a few screen shots from our account:

Personal Capital also gives a great net worth snapshot, which includes ALL of our accounts. Personal Capital talks directly to all your bank and investment accounts and you can input your holdings that are not trackable through online accounts, such as real estate, vehicles, and precious metals.

Best of all, Personal Capital is free. If I only had 1 bank account and 1 investment account, I might not need it, but with several accounts Personal Capital is a no brainer.

What do you think about this $30,000 budget? Have you been able to save money while earning $30,000 a year or less? What advice to you have for other readers?

Leave a Reply