Get A Mortgage Credit Certificate Before Buying A House

You MUST do this before buying a house: Look into Mortgage Credit Certificates (MCCs) in your area. The MCC is a VERY little known about program that can provide a $2,000 tax credit per year (and in some cases more), every year you have a loan on your house. Each state has vastly different laws governing how the Mortgage Credit Certificates work, but for the most part they all follow the same federal guidelines. Mortgage Credit Certificates are issued by states, counties, and cities. It is possible that they might not be available in your area, but are available in the next town over. Offerings are also constantly changing. Several states started MCC programs within the last couple years.

Purpose Of Mortgage Credit Certificates:

The MCC is designed to help lower income households afford to buy a house

The MCC refunds a certain percentage of mortgage interest paid every year through the home buyers taxes. This percentage varies between 20% and 50% depending on the state. For credits over 20% the tax credit is capped at $2,000, for credits of 20% or less, the credit is not capped. I have scoured every inch of the web to learn everything I can about Mortgage Certificate Credits. One of the main points I have found is that the MCC credit only goes into effect after all other credits have been entered.

Breakdown of IRS Treatment of Mortgage Credit Certificates:

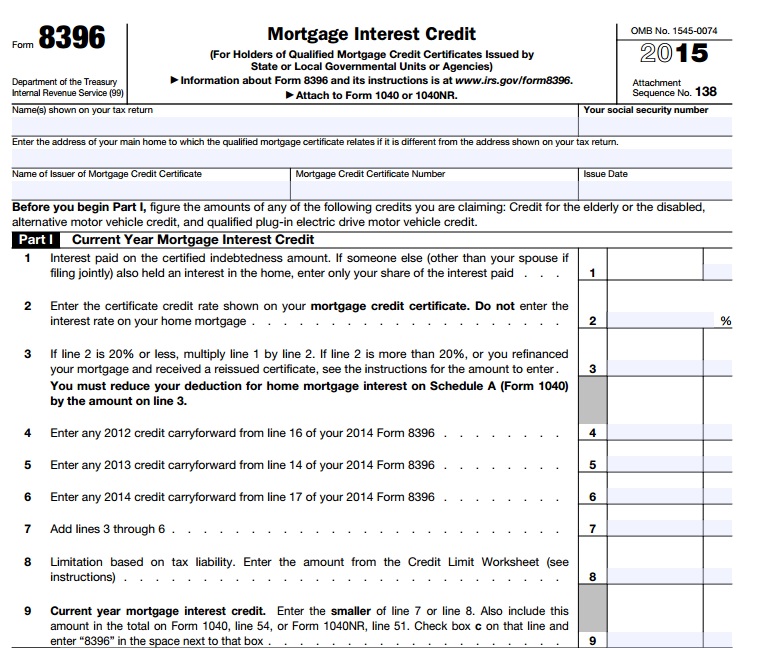

Mortgage Credit Certificates are handled using IRS Form 8396. The form is only 1 page long (with an extra page for instructions) and is really simple to fill out.

- Line 1: Enter interest paid for the year

- Line 2: Enter Credit rate shown on certificate (20% – 50%)

- Line 3: If <20% OR Equal to 20% multiple line 1 X line 2. If over 20%, multiple line 1 X line 2, but write in $2,000 if the total is over $2,000.

- Line 4 – Line 6: Enter any credit carryforward from the previous 3 years.

- Line 7: Add Lines 3 – 6 together

- Line 8: Limit based on tax liability, use Credit Limit Worksheet (on Page 2).; using Form 1040:

- 1. Enter Line 47 (Tax owed after deduction, exemptions, alternative minimum tax, and excess advance premium tax credit repayment)

- 2. Enter Amount from 1040 Lines 48 – 51: (Foreign tax credit, credit for child and dependent care expenses, and the retirement savers tax credit)

- line 12 of the line 11 worksheet in Pub 972 (child tax credit)

- Form 5695 Line 30 (Residential Energy Credits)

- Form 8910 Line 15 (Alternative Motor Vehicles)

- Form 8936 line 23 (Plug In Electric Vehicles)

- Schedule R Line 22 (Credit For Elderly or Disabled)

- 3: Subtract Line 2 From Line 1 Enter this amount on line 8.

- Line 9: Current Year Mortgage Interest Credit: Enter this number on Line 54 on Form 1040, which is labeled “Other credits” and check box C and write in Form 8396.

- (Lines 10 – 17 have to do with carrying forward the MCC)

*Note: This shows that even though the credit is displayed on line 54 of form 1040, it takes into account credits that appear further down on the list. While this credit may not help a lower income family with multiple kids, it can certainly help a moderate income family with a couple kids.

What If You Have No Income Tax Liability?

This credit is valid for 30 years, and each years credit can carry forward for up to 3 years. If in year 1 you have no tax liability, you have until year 4 to claim the credit on your taxes. Many people have their income increase over time, and along with it their tax liability.

As an example, Mrs. C. and I don’t have access to an employer 401K. Between our IRAs and our HSA we can contribute $18,750 per year tax deferred. We also receive $4,000 of child tax credits. With all of these factors, we owe no federal income taxes up to an income of $87,500. If we earned another $10,000 we would owe $1,500 in taxes for the year and be able to start using the tax credit. In 4 years we will also no longer receive the child tax credit for our oldest kid, which will increase our taxes by $1,000 a year. Both of these situations would take us from not being able to use an MCC to being able to take full advantage of one.

Disregarding additional income and tax credit drop offs, it is possible to shift savings from traditional accounts to Roth accounts to qualify for an MCC. The only reason Mrs. C. and I go full traditional at this point in time is to hit a $0 tax liability. By shifting our IRA contributions to Roth IRA contributions we would increase our tax owed and be able to take advantage of the Mortgage Credit Certificate. If we were earning $87,500 and shifted our full $11,000 of IRA contributions to Roth IRA contributions, our tax owed would rise form $0 to $1,650. We could then take up to $1,650 per year in MCC.

Rather than shifting ALL of our contributions to Roth contributions we would calculate out what our actual tax credit would be and then shift that amount of money out of traditional accounts and into Roth accounts. In 2016 we will pay around $4,200 in total interest, giving us what would be a $840 credit. In this scenario we would keep $5,400 of our contributions in the traditional account, giving us a $840 tax liability, which would allow us to fully use our credit, and we would put $5,600 into our Roth IRAs.

Bottom line, I would not use the rationale that today you have no income tax liability, so it doesn’t help to get an MCC. The MCC is fairly flexible and there are actions you can take to take full advantage of the credit.

How Much Money I Left On The Table By Not Using Mortgage Credit Certificates:

I bought my first house in 2006 with an interest rate of around 7.5% on a $47,000 loan with a 15 year amortization. I could have received this tax credit from 2006 to 2011. In 2011 we bought our second home, this one on a 30 year mortgage with a 4.25% rate and a $116,000 balance. Because we live in a “target area” in Michigan, there is not a limitation on repeat buyers, meaning we would have qualified for the credit on this house as well.

- 2006: $3,465 X .2 = $693

- 2007: $3,328 X .2 = $665

- 2008: $3,180 X .2 = $636

- 2009: $3,021 X .2 = $604

- 2010: $2,850 X .2 = $570

- 2011: $3,055 X .2 = $611

- 2012: $4,878 X .2= $975

- 2013: $4,792 X .2 = $958

- 2014: $4,672 X .2 = $934

- 2015: $4,509 X .2 = $901

- TOTAL: $7,547!

And that’s in a state with the lowest rate. If I lived in Ohio I would have had $15,000 over that time period. If I lived in Florida I would have had $17,450. Could you have used $7,500 over the last 10 years? I know I could have. Take the time to look into Mortgage Credit Certificates.

What Does This Tax Credit Mean When Applied To A Mortgage?

Besides making home ownership more accessible one of the goals of the MCC program is to help lower income buyers purchase a more expensive home that they otherwise could not afford. The tax credit received is used as a direct credit against the cost of the home for debt payment to income ratios. If a home buyer can afford a payment of $450, on a 3.5% 30 year mortgage they could buy a $100,000 home. If they received a 50% mortgage credit certificate, they could instead buy a $137,400 home. The $2,000 tax credit would reduce their monthly payment by $167, allowing for a monthly payment of $617 per month.

9 States offer a 50% MCC. With 30 Year mortgage rates at around 3.5%, this effectively means a home buyer would be getting a 30 year mortgage for 1.75% on a home as long as the loan was under $115,000. A Larger mortgage amount would mean that the credit would be “capped” to $2,000 and the effective interest rate would be a little bit higher. In the first year on a $115,000 3.5% mortgage the total mortgage payments would be $6,196. The total interest would be $3,989, making the first year tax credit $1,994.50. This reduces the total cost of the first year mortgage by 32%!!!! Over 30 years, the total of the MCC would be $35,452!

What about a more modest house? In my area a first time home buyer can get a fairly nice place for $50,000. A $50,000 30 year mortgage at 3.5% would cost $2,694 per year, with $1,734 going to interest the first year. A 50% tax credit on the interest would be $867. This would still be 32% of the loan. Over the life of the loan the borrower would receive $15,414 in tax credits.

For a more expensive house, say one costing $225,000 on a 3.5% mortgage the interest would exceed $4,000 per year for the majority of the loan, allowing the home buyer to receive the maximum credit. Over the first 19 years of the mortgage the buyer would receive a $2,000 credit. The credit over the last 11 years of the mortgage would total $11,400, for a grand total of $49,400 over the course of the entire mortgage. The total mortgage cost per year is $12,124. A $2,000 credit reduces this by 16.5%.

NOTE: On states with a 20% credit, it is possible to receive greater than a $2,000 credit per year because the $2,000 limit only applies to states that offer a credit of greater than 20%. Since 13 states offer a 20% credit, I figured this needed to be addressed. With interest rates at around 4% for a 30 year mortgage, to exceed $2,000 in credit, the home buyer would need to pay over $10,000 in interest in the first year, meaning a total loan in excess of $255,000, which is above the max home price in many of these states. Still, in states like California that offer a 20% credit and a maximum purchase price in some counties of $729,635, this is some extremely valuable information. On a $700,000 loan at 4%, the first year interest would be $27,776. 20% of this would result in a credit of $5,555. The other $22,221 could be deducted from taxes as an itemized deduction. Over the life of the loan, the buyer would pay $503,086 in interest, and receive credits totaling $100,617.

Mortgage Credit Certificate Vs. Mortgage Interest Deduction:

The Mortgage Interest Tax Deduction (MID) is what the MCC should be. It is the sacred cow of the American housing market. Not even Rand Paul would cut this out of his proposed budget. The Mortgage Interest tax deduction is essentially a tax break for high income buyers to buy expensive homes. A full 77% of the MID went to taxpayers earning over $100,000 per year.

In 2011 The MID cost over $100 Billion and 34.4 Million people used it. In 2011 guess how much the MCC cost? Just $44.2 million 4/100 of 1 percent of the MID, and only 44,868 people used it. Why? Because NO ONE freaking knows about it! I have been writing about personal finance for 3 years, I have bought 3 homes, and purchased my first house when I was 20. I study mortgages and home ownership for fun. I have analyzed the US Tax Code for hundreds of hours and I have not come across MCCs, until I found them by accident while looking up first time home buyer programs in Michigan for a family member. Building on how unknown these programs are, in April of 2014 in South Carolina only 43 people had taken advantage of the program year to date, that’s well under 200 people for the year, in a state with 4.8 million people.

The MCC is a much more effective tool for making home purchases more affordable than the MID is. Mortgage Credit Certificates target first time home buyers, they target lower income buyers and they provide a tax credit that anyone can take instead of a deduction that can only be used by people who can itemize their deductions.

Borrowers can also use the MCC with the Mortgage Interest Tax Deduction. The portion of the interest that the borrower does not receive a tax credit for can still be deducted. So If I have $3,000 in mortgage interest and receive a $1,500 credit, I can still deduction $1,500 if I choose to itemize my taxes.

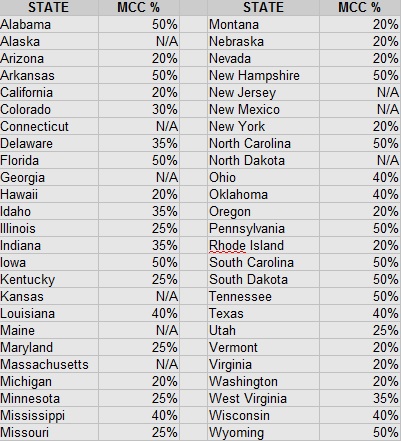

Breakdown of State Mortgage Credit Certificate Programs:

I have been able to find references online to Mortgage Credit Certificate programs in 41 states. I have since contacted the other 9 states and have confirmed that they do not offer Mortgage Credit Certificates. I have linked to the best resources I could find in the state for the MCC programs. Please note that the majority of these links go directly to government sites which have a decent amount of information, while others go to newspaper articles that simply mention the MCC program requirements in that state.

Maximum Mortgage Credit Certificate Rate By State

Further Information on State Mortgage Credit Certificate Programs:

Note: The income limits given here are for general areas throughout the state in designated target areas. Non target areas have slightly lower income limits and have lower house price maximums. All income limits are for gross income of all adults in the household. Follow the links for more information for eligibility requirements in your state. Generally speaking, the sale prices are limited in target areas to $312,361 in target areas and $255,573 in non target areas.

Some counties have different income limitations than others. Across the board all properties must be owner occupied. The program is generally limited to first time home buyers, however most states have “target areas” where repeat buyers can also benefit from the program. Target areas are areas where 70% of families live below 80% of the statewide median area income. Additionally I am providing the maximum home price for single family homes. In many states borrowers can buy multifamily homes with a higher purchase limit.

- Alabama: Can be paired with the Step Up program, or any other 30 year mortgage. 20% credit on loans over $150K, 30% credit on loans of $100K – $150K, and 50% credit on loans under $100K. Income for households of 1 -2 < $66,600, households of 3+ <$77,700 in target areas.

- Arizona: 20% credit across the board, Income for households of 1 -2 <$71,760, households of 3+ <$83,720 in target areas.

- Arkansas: 50% credit, Income limits for households of 1 – 2 < $63,442, households of 3+ $72,958. Maximum purchase price of $250,000.

- California: 20% credit, Income limits vary greatly by county. The highest counties have a limit for families of 1 – 2 people of $140,640 and of $164,080 for 3+ people. Sale price limitations also vary greatly, with the highest counties having a limit of $729,635.

- Colorado: 30% credit. Maximum income $108,920 in target areas, maximum sale price of $467,500.

- Delaware: 35% credit, buyers can also use down payment assistance program. Maximum income for households of 1 – 2 people <$97,320; for households of 3+ $113,540. Maximum purchase price is $357,831.

- Florida: 50% credit, income limits vary greatly by county, for 1 – 2 people from a low of $57,700 to a high of $122,220; For 3+ people from $66,680 – $122,220. Maximum purchase price varies greatly by county, with a max of $609,638.

- Hawaii: 20% credit, maximum income for 1 – 2 people of $120,600, for 3+ $140,700. Maximum purchase price of $679,879.

- Idaho: 35% credit. Maximum income is $90,000, except Blaine Co. which is $110,000. Maximum purchase price $312,300.

- Illinois: 25% credit. Maximum income for 1 – 2 people; $91,200, for 3+, $106,400. Maximum purchase price $426,585.

- Indiana:Credit varies between 20% and 35%. Can be used with down payment assistance program.

- Iowa: 50% credit. $316,000 Maximum purchase price.

- Kentucky: 25% credit. Income limits for 1 -2 people; $84,840, for 3+ $98,980. Maximum sale price of $255,500.

- Louisiana: 40% credit. 1 – 2 person income limit $66,960; 3 person limit $78,120. Maximum house price $305,800.

- Maryland: 25% credit. Income limits and home sale prices vary by county. Highest are 1 -2 person income limit of $131,320, 3+ people income limit of $152,040. Maximum home sale price of $525,091.

- Michigan: 20% credit. Statewide general income limits are $75,000 for 1 – 2 people and $87,500 for 3+. The highest county rates are $109,920 for 1 – 2 people, and $128,240 for 3+. Maximum sale price of $224,500.

- Minnesota: 35% credit. Income limits for 1 – 2 persons: $86,600, for 3+ $99,500. Maximum sale price of $298,125.

- Mississippi: 40% credit. Income limits vary by county. Highest are 1 – 2 people $69,840, 3+ people $75,320.

- Missouri: 25% credit. Income limits vary by county, maximum for 1 – 2 people $87,960, 3+ $102,620. Maximum purchase price $312,368.

- Montana: 20% credit.

- Nebraska: 20% credit. Income limits vary by county, with maximum for 1 – 2 persons being $83,880 and for 3 + people $97,860. Maximum home price $235,000.

- Nevada: 20% credit.

- New Hampshire: 50% credit for homes under $50,000, 30% credit for homes over $50,000. Income limits for 1 – 2 people $99,000; for 3+ people $115,500. Purchase price limit of $320,000.

- New York: 20% credit.

- North Carolina: 30% credit on existing homes, 50% credit on new construction. Can use with NC Home Advantage Mortgage. Income limits vary by county. Typically $64,000 for 1 – 2 people and $74,000 for 3+.

- Ohio: 40% credit when used with OHFA First Time Homebuyer program. When purchased outside this program credit is 30% for a bank owned property, 25% for properties in a target area, and 20% for all other properties. Income limits vary by county. Typically $73,080 for 1 – 2 people and $87,640 for 3 + people.

- Oklahoma: 40% credit.

- Oregon: 20% credit. Appears to only be for the city of Portland. Income limits for 1 – 2 people $73,300, for 3+ $84,295. Maximum purchase price of $373,658.

- Pennsylvania: 50% credit. Income limits for 1 – 2 people vary by county, highest are for 1 – 2 people $97,300, for 3 + $113,500.

- Rhode Island: 20% credit Income limit of $89,280 for 1 – 2 people, $104,160 for 3 + people. Maximum home price of $407,195.

- South Carolina: 50% credit. Limits vary by county. Highest income limits for 1 – 2 people is $82,680, for 3+ $96,460. Maximum sale price of $295,000.

- South Dakota: 40% – 50% credit. Income limits vary by county. In target areas the limit is $75,480 for 1 – 2 people and $88,060 for 3+ people. Maximum sale price is $305,800.

- Tennessee: 50% credit. Income limits vary by county. Highest is $82,200 for 1 -2 people, $95,900 for 3+ people. Maximum sale price of $375,000.

- Texas: 40% credit.

- Utah: 25% credit. Highest income limit is $137,200.

- Vermont: 20% credit. Can be combined with a VHFA first mortgage program. Maximum income limit for 1 – 2 people is $95,000, for 3+ is $110,000. Maximum purchase price is $300,000.

- Virginia: 20% credit. Maximum income limit for 1 – 2 people is $121,900 and for 3+ people is $142,300. Highest maximum purchase price is $500,000.

- Washington: 20% credit. Highest income limits for 1 – 2 people is $90,000 For 3+ people is $97,000. Highest purchase price limit is $475,000.

- West Virginia: 35% credit.

- Wisconsin: 25% credit for non target areas, 40% credit for target areas. Maximum income limit of $86,600 for 1 – 2 people, for 3+ $99,590. Maximum purchase price of $417,000.

- Wyoming: Credit can be from 10% to 50%.

IRS Mortgage Credit Certificate Tax Recapture:

As with all good things there is a catch. In the event that the house is sold in under 9 years, and it sells for a gain, the federal government can recapture a portion of the tax credits that have been received over the years. To calculate the tax, you first find out the sale price of the home and then subtract out all closing fees, including realtor fees. The gain between this number and the original purchase price of the home is what is subject to tax. This number is then cut in half. The total tax can not be higher than 50% of the gain.

Next the form has you enter your Adjusted Gross Income, not including any gain from the sale of the house. This number is then compared to the income limits for the MCC under the program. If your income is less than this number, you owe no tax. In a year where you may be subject to the recapture tax it may make sense to increase 401K, IRA, and HSA contributions to reduce your AGI. If your income is $5,000 above the qualifying income amount, then you enter 100 on the next line. If it is under $5,000, then divide the number by $5,000 and enter that percentage on the next line.

At this point the form has you enter the ‘federally subsidized’ amount, which is 6.25% of the original loan amount. In the case of a $100,000 loan this would be $6,250. Then the form has you evaluate how long you have owned the home and assigns a discounted percentage based on this time. The subsidized amount is then multiplied by the holding period percentage, and the total tax owed is either this number, or 50% of the gain on the sale, whichever is less. For more details on how the recapture tax is calculated, check out IRS Form 8828.

Many states have recapture tax reimbursement programs to alleviate the concern home buyers may have for paying this tax in the future if they need to sell their homes.

Are you a participant in the Mortgage Credit Certificate program or do you know someone who is? What do you think of the program, do you think this is a better way to subsidize mortgages than the Mortgage Interest Tax Deduction? For more tips on buying a home, check out The Complete Idiot’s Guide To Buying A House.

Leave a Reply