Marriage Penalty or Windfall?

I don’t think that getting married should affect your tax situation either way, but our tax code is a monster containing many latent effects from numerous revisions and additions over time. How much of a difference can getting married actually make in your tax return? It depends mostly on how extreme the situation is. Below are a couple interesting examples.

I don’t think that getting married should affect your tax situation either way, but our tax code is a monster containing many latent effects from numerous revisions and additions over time. How much of a difference can getting married actually make in your tax return? It depends mostly on how extreme the situation is. Below are a couple interesting examples.

Getting Married Cost Us Thousands of Dollars A Year:

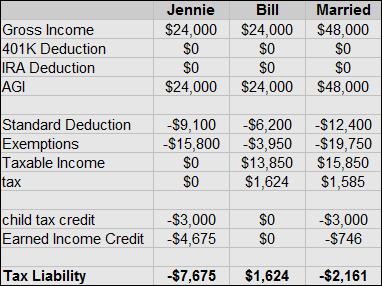

Jennie is a single mom with 3 kids, She works full time and Earns $12 an hour, not bad, but certainly not great. This works out to $24,000 a year. She is dating Bill and they are considering getting married. Currently when they file their taxes Jennie gets a net refund of $7,675, and Bill pays in $1,624. Combined this is a total refund of $6,051. If they were to get married, and their incomes stayed the same, then their refund would be $2,161, a marriage penalty of $3,890.

Jennie is a single mom with 3 kids, She works full time and Earns $12 an hour, not bad, but certainly not great. This works out to $24,000 a year. She is dating Bill and they are considering getting married. Currently when they file their taxes Jennie gets a net refund of $7,675, and Bill pays in $1,624. Combined this is a total refund of $6,051. If they were to get married, and their incomes stayed the same, then their refund would be $2,161, a marriage penalty of $3,890.

Of course together as a household they would be much stronger financially. By combining home and utility expenses both Bill and Jennie would see an increase in discretionary income. Once again though, the number one rule of economics is that people respond to incentives, and a roughly 8% total income pay cut may be incentive enough to cause people to not get married.

Deciding not to get married based on tax reasons might make sense in the short term for some people, but over the long run could have some large financial consequences. What if for instance, Jennie passed away? Although Bill would have physical custody of the children at the time, he would not have any legal standing for keeping the kids, and the court system may give them to their non-custodial parent, or perhaps worse put them in foster care. What if something happened to Bill instead? The family had grown used to his income, but since he wasn’t married Jennie would not receive any Social Security survivor benefits. Did Bill have life insurance? If so did he name her as a beneficiary? When they do get married Bill should aim to adjust his W4 form and claim exempt on federal withholdings, because combined they will owe no federal income tax.

Getting Married Saved Us Thousands of Dollars A year:

What if instead of having 2 moderate income earners joining, we have one high earner joining a non-earner?

What if instead of having 2 moderate income earners joining, we have one high earner joining a non-earner?

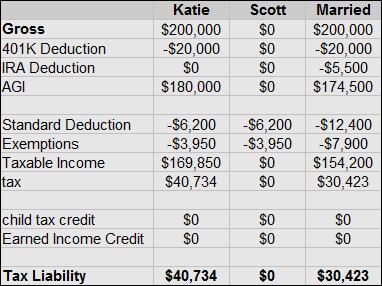

Katie is a Doctor and earns $200,000 a year. Her long term boyfriend Scott stays home to take care of their 3 dogs and plans on being a stay at home dad when they have kids in the near future. They are not married. Katie contributes 10% of her earnings to a 401K plan and ends up paying $40,734 to the IRS. Scott has no earnings and so he doesn’t pay in anything. Because Scott has no income he can not contribute to a retirement account. If he was married to Katie they could contribute $5,500 to a spousal IRA. Getting married would also allow Katie’s income to fill Scott’s lower tax brackets, which are currently empty. As a married couple they would pay $30,423 in income tax, a reduction of over $10,000.

Deciding to get married for tax reasons may be as short sighted at not getting married for tax reasons. A savings of $10,000 a year is nothing to snear at, but at the same time, making major life decisions over $10,000 isn’t the best way to go through life.

Conclusion:

As I previously stated, tax consequences should not drive the decision making process, but they do need to be considered. Jennie and Bill would have to take a serious look at their budget and plan for the cut in income for when they decide to get married. Even though all of Scott’s earnings on top of Katie’s if they decided to get married would be taxed at 40% (28% Federal plus 7.65% Payroll taxes and 4.32% state tax in MI), it might be in his best interest to have his own earnings record for Social Security to cover himself if him and Katie don’t stay married for at least 10 years. Even though the number one rule of economics is that people respond to incentives, we must as individuals decide which incentives are the right ones to respond to, and how they affect us in both the near and long term.

Would you consider adjusting major life plans based on tax consequences?

Leave a Reply