How To Calculate Your Taxes In 2018

I do a lot of planning for my taxes, so much so that it feels obsessive at times. A few years ago I made a tax planning spreadsheet that allowed people to compare side by side different tax scenarios. This greatly simplified my tax planning, and helped many others as well. I didn’t update it for 2017 as updating the calculations is a pain in the butt and the changes were very minimal. As everyone who doesn’t live under a rock knows President Trump just signed into law the largest tax change bill in a generation.

There’s a ton of ink written on the changes already, as a summary, personal exemptions are completely gone, the size of the standard deduction has greatly increased, tax brackets are completely changed, the child tax credit doubled, and the refundable portion increased from $1,000 per kid to $1,400 per kid.

Here’s an overview of what my spreadsheet does to calculate your taxes in 2018:

To itemize or not to itemize?: This sheet lets you list out your potential itemized deductions and adds them up. If it’s below the standard deduction amount it will automatically input the standard deduction in the tax calculations sheets, if it is above the standard deduction it will input your itemized deductions in the tax calculation sheets.

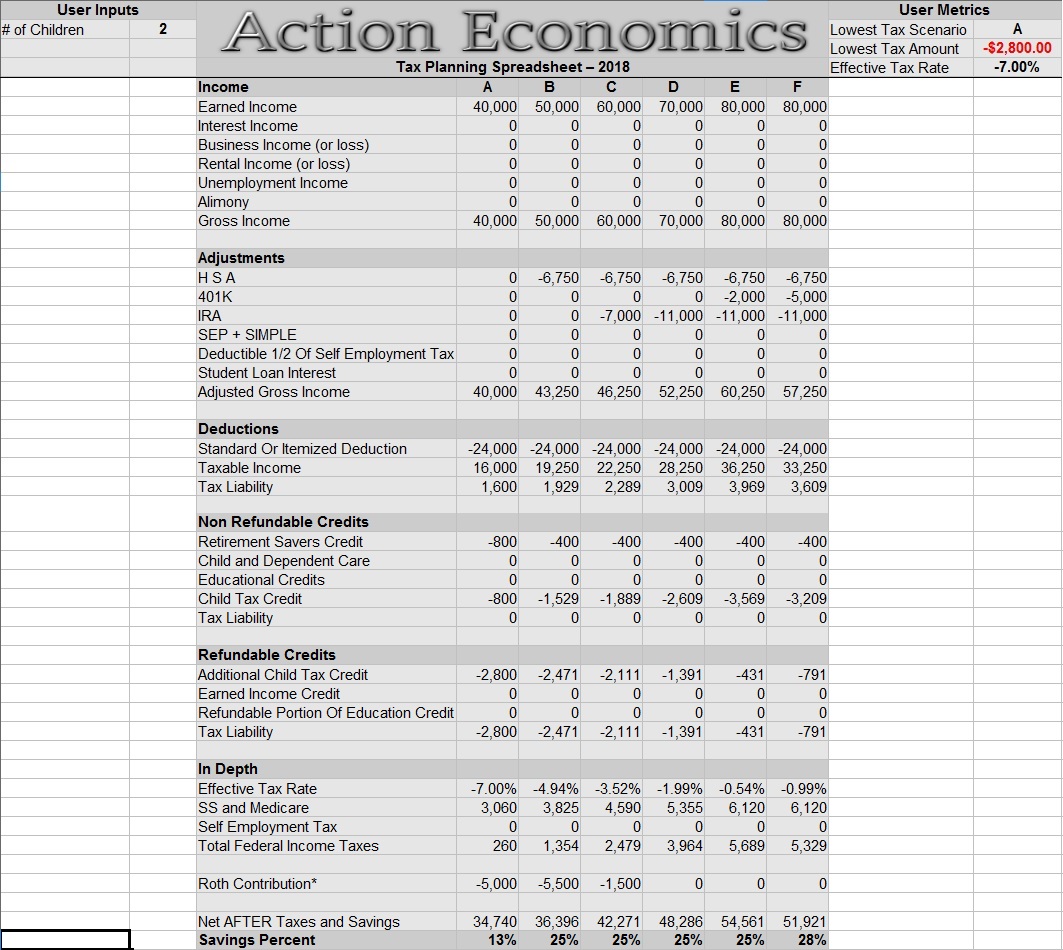

Compare 6 scenarios side by side: This is the main feature of this spreadsheet. These comparisons allow you to maximize your tax efficiency. There is a separate sheet for each filing status. I think six is about the right amount of comparisons. Generally I will compare 3 different income amounts across 2 different strategies for deploying retirement savings.

Calculate Tax Credits: This spreadsheet calculates the child tax credit, additional child tax credit, and the retirement savers tax credit, with all calculations updated for tax year 2018. In a future version I may add it an earned income credit calculation, however this has proven extremely difficult for me to turn into a reliable calculation. For now I recommend using the Earned Income Credit calculator at Bankrate.com, and then inputting that number into the spreadsheet.

User Metrics:

Under the User Metrics section this spreadsheet will identify which of the 6 scenarios gives the best refund, what that refund amount is, and what your effective tax rate is.

In Depth Calculations:

Not only does this spreadsheet calculate your federal income tax and effective tax rate, it also calculates your self employment tax, social security and medicare tax, and a total Savings rate as a percent of gross income by adding up 401K/IRA/HSA/and Roth contributions.

So What Does The New Tax Bill Mean For Me?

Mrs. C. and I should receive a refund of around $4,141 for tax year 2018, as opposed to a refund of $1,085 for tax year 2017. This change is almost completely due to the changes in the child tax credit. Since the child tax credit doubled from $1,000 per kid to $2,000 per kid, we ended up with a much larger refund that was able to offset the loss of the exemptions and put an extra $3K in our pockets. This is for a family of 6 with an AGI of $62,620.

How Might This Tax Bill Change My Strategies?

1. More money into traditional retirement accounts: I like to look at the back end when deciding how much money to put into traditional vs. Roth accounts. Previously a married couple would have roughly the first $20,800 of income tax free and the next $18,650 at 10%. Under the new tax bill the first $24,000 of income is tax free and the next $19,050 is at 10%. If using a 4% withdrawal rate in retirement under the previous tax regime you would want $520,000 in traditional accounts to fill the 0% bracket, and probably another $466,250 to fill the 10% bracket. Under the new system you would want $600,000 in traditional accounts to fill the 0% bracket and another $476,250 to fill the 10% bracket.

2. Once the house is paid off invest more in Roth or Taxable accounts instead of putting all my money in traditional tax deferred accounts. I am planning to have our house paid off at the end of 2020. To some extent this contradicts point 1 above. Using my spreadsheet I was able to find that for a family with 4 children once you hit an AGI of $50,500 your refund will not increase. This is because the refundable limit on the child tax credit is $1,400 each. Between the retirement savers tax credit of $400 and the child tax credit this is the AGI in which you “max out”.

For 2017 we saved $38,000 and if we had our house paid off would have saved another $7,000 for $45,000 in total savings. With an estimated $86,000 in gross earnings we could contribute $35,500 to traditional accounts to reach an AGI of $50,500. It would then make sense to deploy the additional $9,500 in savings into Roth accounts. We could then use the $5,600 in federal tax refunds to fund our taxable brokerage accounts.

Note: Although taxes don’t change for a family of six below an AGI of $50,500 (when maxing out retirement savers tax credit), There may still be a reason to contribute more to traditional tax deferred accounts. If your kids are going into college and you can hit an AGI of under $50,000 this is something you will want to do. If your AGI is below $50,000 then you are exempt from the assets test for financial aid.

Preparing For Only 3 Kids:

To receive the child tax credit the child must be under 17 at the end of the year. This means the last year our family will have 4 kids that we get the credit for will be 2020, which means we most likely won’t have a year where the above applies. Instead the maximum AGI we will want for a family with 3 kids is $45,500 which would require $40,500 of traditional savings and then putting the remainder in Roths and taxable accounts.

There is absolutely no way I would have figured out how to optimize my taxes in this way without using this spreadsheet. You can download this spreadsheet here.

What do you think of the new tax law? How do you see the new tax rules affecting your life and finances. Also, if you have used my spreadsheet any feedback on potential improvements?

Update: I have been able to successfully change the spreadsheet from OpenOffice to Excel format so the conversion issues discussed in the comments thread bellow should no longer be an issue.

Leave a Reply