How Cheap Are Mortgages When Treasuries Go To Zero?

Across the world, the interest rates on Treasury bills have turned negative in many different countries. In this bizarre scenario, depositors pay the bank to hold on to their money, rather than the bank paying them interest. Such a scenario is obviously not good for depositors, but what about borrowers? Since capital to the banks is better than free, then the cost to borrow money must also be extremely cheap. Here are some of the best examples from around the world.

Germany:

Following Brexit, many European debt yields, which were already near 0 turned negative. In Germany, a 10 year mortgage has a rate of 1.04% and a 30 year mortgage has a rate of 2.21%. This is some great news for potential first time home buyers. Germany currently has a home owner rate of only 43%.

Japan:

Japan began using negative interest rates at the start of 2016, with rates on excess deposits being -.1%.

In Japan, borrowers can get a 35 year mortgage for 1.1%. A 10 year fixed rate mortgage can be had for 0.55%. In terms of U.S. Dollars, this means a $100,000 35 fixed rate loan would have a mortgage payment of $297. The total interest paid over the life of the loan would be $20,527. For a $100,000 10 year fixed rate loan the payments would be $856. The total interest paid over the life of the loan would be an amazingly low $2,798.

Those countries all have amazing rates, but what about negative rates?

Denmark:

In Denmark Mortgages in some instances have gone negative. This is because some adjustable rate mortgages are tied to the LIBOR rate. When the LIBOR rate goes negative, it is possible for mortgages to go negative as well. A common term is LIBOR + .7%. Although this prevents adjustable mortgage holders from paying interest, and indeed leads to a small interest payment due to the borrower, the borrower still has to make their principal payment.

What About The United States:

Currently the U.S. 10 year Treasury Bill is at 1.55%. This overall is extremely low. There is talk that the 10 year rate could hit below 1%, and our Federal Reserve Bank has not taken negative yields off the table. I see this type of currency manipulation as a bad thing that leads to bubbles and destroys the value of our money, but I don’t get to set monetary policy. As depositors, including individuals, institutions, and governments seek safety for their money, they will flock to U.S. Treasuries, which will put downward pressure on the notes. This will in turn have noticeable affects on the US mortgage industry and provide an amazing opportunity to refinance or buy a house at amazingly low interest rates.

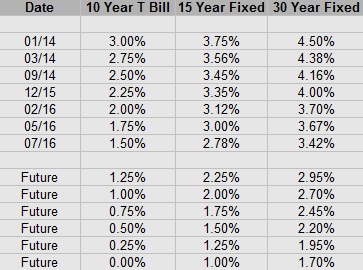

Spread Between 10 Year T Bill and Mortgage Rates:

Mortgage rates don’t follow the T Bill price exactly, but they do trend with it. Overall, the 30 year mortgage stays about 170 basis points over the 10 year T Bill while the 15 year fixed rate mortgage stays around 100 basis points over the 10 year T Bill. So what will rates look like if the 10 year T Bill continues to Fall?

One aspect of lending that is apparent here is that as rates get lower, the spread seems to increase. This is because banks become increasingly hesitant to lend money long term at such low rates. Currently the spread on the 10 year T-Bill and the 30 Year mortgage is around 200 basis points, instead of the norm of 170 basis points.

Will Treasuries Go To Zero?

There are people on both sides of this argument, and in all honesty, no one knows for sure. What I do know is that it is important to prepare yourself to take advantage of an opportunity should it arise. During the first week of July my credit union offered a 5/1 ARM at 2% with .325 points due at closing. This was an amazing offer that only lasted for two days. Since I am off work right now a refinance would be impossible. I am getting everything ready for a refinance so that I can pounce if and when rates drop again. If rates on T Bills truly do fall below 1% we could see 15 year mortgages below 2% and 30 year mortgages below 2.75%. If treasuries go to zero in the U.S. it would be more of a result of the Federal Reserve moving into negative rates than market forces. Either way, it is something we should all be prepared for.

How To Prepare:

If interest rates drop substantially you will want to be able to take advantage and lock in a rate at a moments notice. When rates drop they might not stay low for very long. I have build a binder with all of my documents in it, so that I don’t have to spend hours assembling documentation for lenders when I need to shop for a refinance.

1. Compare your current amortization to a refinanced amortization to see how much cash you would save. I use my Mortgage Spreadsheet to do this. In my situation, a refinance will save me around $7,500 once I go back to work, even with my aggressive goal of paying off my house in 5 years. The higher your mortgage balance and longer you plan on keeping the loan the more important a refinance is.

2. Stock Cash: Be ready to pay around $3,000 in total closing costs. Although it is possible to roll closing costs into the loan it is better to pay for them as you refinance.

3. Gather Documents: For a refinance you may need:

- 2 Years of tax returns and W2s

- 6 months of bank statements

- Recent statements for IRAs, 401Ks, HSA’s and other assets.

- Statements of all debts owed, credit cards, car loans, student loans, mortgages etc.

- 1 month of check stubs: The bank wants to know you are employed and what you make. For someone who works for multiple employers like myself, I keep my most recent full month of checkstubs from all 3 of my employers and have a note written explaining my employment situation to the underwritters.

- Most recent Title Insurance: You may be able to save a bit of money on the banks title insurance if it hasn’t been very long since you bought or refinanced your house.

Where do you think U.S. T Bill’s and interest rates in general are headed? I personally thought 2 years ago that we had seen the last of low interest rates, boy was I wrong. It will certainly be interesting to see what happens over the next 6 months to a year.

Leave a Reply