Help With Buying A First House

Buying a first house

There are ways to buy a first house without a 20% down payment and there are several ways to get help with buying a first house. When looking at all the options, if you are unable to put down a 20% down payment stay conservative with your home purchase and ensure the cost of your home is under 200% of your yearly income and get a loan term of 20 years or less that has monthly payments equal to less than 25% of monthly income.

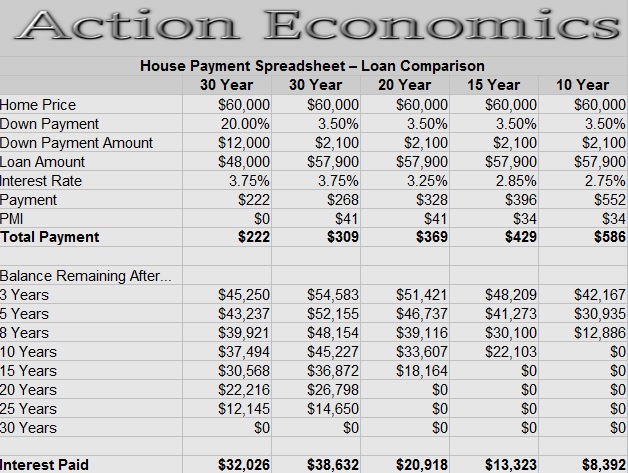

Consider this: Getting a 10 year, a 15 year, or even a 20 year mortgage with only 3.5% down still ends up being a better mortgage product than a 30 year mortgage with 20% down. It takes a 10 year mortgage less than 3 years to catch up on equity built to a 30 year with a 20% down payment. It takes a 15 year mortgage under 5 years and a 20 year mortgage only 8 years to establish more total equity than the 30 year mortgage with 20% down. The 20 year mortgage will pay only 65% of the interest of a 30 year mortgage, the 15 year mortgage will pay only 41%, and a 10 year mortgage will pay only 26% of the interest of a 30 year mortgage with a 20% down payment.

The length of the loan amortization is more important than the down payment. If you are ready to buy your first house with everything but a large down payment, and are willing to get a modest home on a short loan, these can be some great options to get in a house much sooner.

Mortgage Products To Help With Buying A First House:

There are several mortgage products designed to help people buy a first house. The FHA, The USDA, and the VA all have programs that offer low down payment loans. Be careful though and read the fine print, all of these loans come with extra fees that conventional loans do not.

FHA Loans:

FHA loans can be for 15 years, 20 years, 25 years, or for 30 years and only require a 3.5% down payment. FHA borrowers must pay a 1.75% insurance cost upfront when closing on the loan. The fee can be rolled into the loan. It is also common for borrowers to ask the sellers to pay for some of their closing costs. Do not be afraid to ask for closing cost assistance, especially if a home has been on the market for a while and you are making a decent offer.

FHA loans also come with ongoing insurance costs, which depend on the down payment and loan term. Until recently mortgage insurance through FHA would be cancelled when the loan to value (LTV) ratio hit 78%. This changed in 2013. Now any loans with less than a 10% down payment must pay mortgage insurance for the duration of the loan. For borrowers who put down 10% or greater the premium is “only” charged for 11 years. This premium varies from .45 to 1.05% of the loan each year depending on the initial mortgage amount, duration, and loan to value.

USDA Rural Development Loans:

USDA rural development loans exist to encourage people to move to less populated areas. USDA rural development loans are available in 15 year and 30 year terms. These loans require no down payment, however they come with a 2.75% upfront insurance premium. This premium can be rolled into the loan amount. There is also an ongoing fee of .5% of the loan value per year. Starting in October of 2016 these fees will drop substantially. The upfront insurance fee will drop from 2.75% to 1%. This is a game changer.

When Mrs. C and I purchased our current home we were offered a USDA rural development loan as an option, but I balked at the 2.75% upfront fee, which was about $4,000. With the new fee structure coming in October, the USDA loan is much more appealing. The fee for a $150,000 home would only be $1,500 which is much easier to stomach than $4,000. The ongoing fee will also drop from .5% to .3%. For a $150,000 home this is a reduction from $750 per year to $450 per year.

VA Loans:

VA loans are for veterans and current members of the armed forces. VA Loans are 0% down payment loans that do not require an ongoing mortgage insurance fee. There is an upfront insurance fee of between 1.25% and 3.3%. This upfront funding fee is waived for any applicants who are received a 10% or greater VA disability payment. The funding fee can be rolled into the loan amount or the buyer can ask the sellers to cover some or all of it.

With all of these loans closing costs and interest rates can still vary greatly. Make sure to shop around multiple lenders before making a decision. When we got our last mortgage I had lenders detailing closing costs that varied from a low of around $1,800 to a high of over $5,000! Lending Tree is a great place to start to get quotes from multiple lenders.

Programs To Help With Buying A First House:

There are several first time home buyer programs that are available, however most of them come with strings attached and the vast majority of them are either state based or even based on a specific local area.

HomePath:

This is a Fannie Mae program designed to offer first time home buyers the option to buy bank foreclosed properties before investors are given an opportunity. The Homepath program requires potential buyers to go through an online home buying course which costs $75. Successful buyers can receive up to 3% of their home value to pay for closing costs through this program. On a $50,000 home that is $1,500.

This is a Michigan only program, although other states I’m sure have similar programs. With this program first time home buyers in Michigan can receive up to 4% down payment assistance up to $7,500. Effectively this program exists to make it so buyers can purchase a home in Michigan with no money down when used in conjunction with an FHA loan. There are income limitations that vary by county. In my county, Berrien County the limit is $75,000 for a family of 1 -2 and $87,500 for a family of 3 or more. There is also a limit on the cost of the home being purchased, which is $224,500 across the board. A minimum credit score of 640 is also required. This program has also been expanded to allow for current home owners to benefit through the MI Next Home Program, which also includes the same down payment assistance. I certainly wish I knew about this program when Mrs. C. and I bought our house, we would have saved $5,800!

Note: The down payment assistance is attached to the property as a “soft second” loan. It gains no interest, has no payments, and only has to be paid back when the house sells, the owner refinances, or when the owner pays the house off in full.

Michigan IDA:

This program is a savings account matching program designed to encourage home ownership. For potential buyers with income in a certain range, the state of Michigan will match savings for a down payment at a rate of $3 for every $1 saved, up to $1,000 of personal savings, for a total benefit of $3,000. With $4,000 saved a home buyer could easily get a $60,000 home and cover the 3.5% down payment and the vast majority of the closing costs with this money. This program is funded through both public and private funds.

Program participants must be below 200% of the Federal Poverty level or qualify for Earned Income Credit, and total household net worth must be under $10,000. The matching funds are kept in a separate account until the home purchase is made.

Mortgage Credit Certificate:

The Mortgage Credit Certificate or MCC, is a program that gives first time home buyers a tax credit for mortgage interest paid. In Michigan this credit is limited to buyers who have not owned a home in 3 years and are buying the home as a principal residence, unless they live in certain counties that are “targeted areas”, my county, Berrien, is one of these areas. One major string to this program is that if the home is sold for a profit in under 9 years of home ownership, the Federal Government will recapture some or all of the MCC’s received.

Michigan allows a 20% MCC credit, so on a $50,000 loan at 4% interest this would amount to a $400 tax credit for the first year alone. Each year would be a bit less as the total balance reduces. Other states have different credit levels. Texas for instance has a 40% credit level, while Florida has a 50% credit. On the same $50,000 loan at 4% interest the Texas credit would be $800 and the Florida credit would be $1,000.

This credit is non-refundable and can only be used to reduce tax liability after other credits and deductions are used, through line 51 on Form 1040. The child tax credit, earned income tax credit, and the american opportunity tax credit do not reduce this credit. This credit is valid for EVERY SINGLE YEAR of the loan. The same income limits apply as for the MI First home program. There is a $2,000 per year federal limit on MCCs if the state offers a credit greater than 20%. One really nice feature of this tax credit is that it can be carried forward for up to 3 years. This is great if you have a year or two where you get your tax bill down to $0 and can’t take advantage of it.

Once again, I wish I had known about this program before we bought our last house. We would have saved close to $5,000 to date on taxes. MCCs are also a REALLY great way to get your taxes owed to $0, resulting in the ability to claim exempt on your W4 form. To get MCCs you need to sign up for it when you get your home from a lender who participates in the program.

Habitat For Humanity: Habitat For Humanity

Getting Help With Buying A First House Bottom Line:

If you are in a good financial position, with a stable work history, it is possible to buy a house without 20% down, but it is imperative that you select a modest house costing no more than 2 times your annual income on a 20 year mortgage or less. Check out my article Checklist For First Time Home Buyers for more aspects of buying a house to look at. Many of these programs can be combined with others, so check with your potential lenders when shopping for a mortgage.

If you already own your home how did you buy your first home? If you aren’t a homeowner yet, what is holding you back?

Leave a Reply