Why You Shouldn’t Worry About Investment Returns

All too often people ask me what they should invest in. Many are worried about trying to pick the next best stock and find a way to “make it big” in the stock market. This isn’t how wealth is built and this is a major problem in thinking in terms of priorities for someone who is starting to build a nest egg. In reality returns matter very little until a substantial nest egg has been built up over several years.

A Matter of Perspective:

Depending on what stats you look at “the stock market” has returned between 7% and 12% between 1926 and 2015. Anything in between these numbers is a fairly realistic estimate of what one could receive in returns. With that being said, there are many different ways to invest in the stock market. These figures typically are following ONLY the S+P 500, which is composed of only large U.S. companies. investing in international stock mutual funds and small and medium cap US funds would generally increase returns over the long run. For the purpose of this article, lets use 7% as our low and 12% as our high.

Math:

Let’s say that Joe earns $50,000 per year and saves $2,000 per year. So far he has amassed $10,000 in savings. A 7% return on this is $700, a 12% return is $1,200, and an amazing 15% return is $1,500. These are not life changing amounts of money. Yes these sums compound over time, but that only works well if you start really early and have a time horizon of several decades. In order to get higher returns Joe most likely would take on a LOT of extra risk and spend a lot of time learning about the “best” investments for right now to get that return.

You know what would be MUCH easier? Saving more money. Not only is saving more money easier, it also carries zero risk, there is only upside. If Joe earned 10% more and spent around 10% less, he would save another $10,000 each year, increasing his total yearly savings by around 600%.

Joe saving $2,000 per year and getting 12% sustained returns would take over 5 decades to catch up to Joe saving $12,000 per year and getting 7% returns. Also, chances are extremely low that Joe could sustain 12% returns over such a long period of time. If you want to reach financial independence, increasing your savings rate matters far more than investment returns.

Savings/Returns 5YR 10 YR 15YR 20YR 25YR 30 YR 50 YR

2K/Year 12% $14,173 $39,151 $83,172 $160,751 $297,473 $538,422 $5,376,147

12K/Year 7% $73,839 $177,403 $322,656 $526,382 $812,117 $1,212,876 $5,219,831

Between the time I was 18 and 22 I was focused solely on market returns because in the position I was at the time, it seemed really difficult to save money. I was invested across 3 individual stocks, with an amazing $1,000 each. One of those stocks barely moved, one of them lost about 30% in value and one of them doubled in value. A 100% return on a $1,000 investment is still only $1,000 and doesn’t move the needle much. Also, the amount of risk that investing in an individual small cap stock has is extremely high, especially for a third of one’s portfolio. Since then I have certainly learned that savings rate matters far more than investment returns.

Examining Risk:

One measure of risk is standard deviation. Standard deviation is a measurement of how much a data set fluctuates over time. Something with wild swings has a high standard deviation and something with fairly small changes has a low standard deviation. The higher the standard deviation, the more at risk your money is.

Here are some examples of the standard deviation of different funds and their 10 year annualized returns;

Fund Class Standard Deviation 10 Year Annualized

- Short Term Federal Fund .98 3.00%

- High Yield Tax Exempt Government Bond Fund: 2.93 5.13%

- High Yield Corporate Bond Fund: 4.60 6.71%

- Wellington Fund (65% stock 35% bond): 7.09 7.23%

- S+P 500 : 10.71 7.23%

- Vanguard Small Cap Index Fund 13.11 8.45%

- Health Care Sector Fund 13.77 10.68%

- REIT Index 15.37 6.49%

- Precious Metals and Mining 34.99 -1.98%

Precious metals are a great example here. For 2016 the Vanguard precious metals and mining fund is up an amazing 79%, but over the past 10 years it is at a 2% annualized loss. Market timing does not work. By the time the vast majority of investors realize gold is going up (or anything for that matter) it is generally too late. Most of the gains have already occurred and the buyer gets in at the right time to pay a high price and then lose money when the valuation goes down.

Over a 10 year period the precious metals and mining stock had 4X the risk of the Wellington fund, and ended up with an annualized return 9% less than the “boring” Wellington fund, and that includes this years 79% jump!

Another great example is the balanced fund with 65% stocks and 35% bond allocation. This fund has 70% of the risk as the S+P 500 fund, and has given the same annualized return.

Now, a very important rule of investing is that past performance is no indication of future results. Just because these investments performed this way in the past does not mean that they absolutely will in the future. What we do know is that diversification reduces risk, that market timing does not work, and that dollar cost averaging is an excellent tool that overall boosts returns in the long run by forcing you to buy fewer shares when prices are high and more shares when prices are low.

Focus On What You Can Control:

There are three major factors that influence the accumulation of a retirement nest egg: contributions, time, and returns. If you have an extremely long time horizon, say 45 years, you can save as little as $250 a month and even with an extremely low return of 5%, you could have $500,000. If you have decided, like I have that you want your time horizon to be short, then you have to be strong in the only other category you can control, your savings rate.

If your time horizon is 15 years and you want to save only $250 per month, like the guy with a 50 year time horizon, you would need 27% annualized returns…not gonna happen. Increasing your savings 4 fold to $1,000 per month would still require a 12% annualized return to reach $500,000….once again, most likely not going to happen. You would need to save $1,500 per month to hit $500,000 in 15 years with a 7.4% annualized return, which just about matches the 10 year return we have for the Wellington Fund and the S+P 500 fund.

There is an additional bonus that comes with choosing to have a short time horizon, the rate of return has a much lower impact on your overall wealth. For example, if Joe saves $1,500 per month for 15 years and instead of getting a 7.4% return, he under performs by 2% and got a 5.4% annualized return, he would have $421,000 a full 84% of his goal. On the other hand if Joe had a 45 year time horizon and saved only $250 per month, and he under performed his 5% goal by 2% and got a 3% return he would have only $286,000. This is only 57% of his goal. By focusing on saving more instead of worrying about returns and giving yourself a multi-decade time frame, you reduce your risk associated with market returns.

So What Should I Invest In?

I firmly believe that 95% of your effort should be on maximizing your savings rate. Very little of your time and effort should be going into analyzing and picking investments. I only recommend investing in index funds. Since different parts of the stock market carry different risks, it is a good idea to be invested across multiple index mutual funds. The absolute easiest way to get started investing is to set up an account with Betterment. There is no better way to get started. You can open an account and start investing with only $100. You will instantly be invested across several different Vanguard index funds.

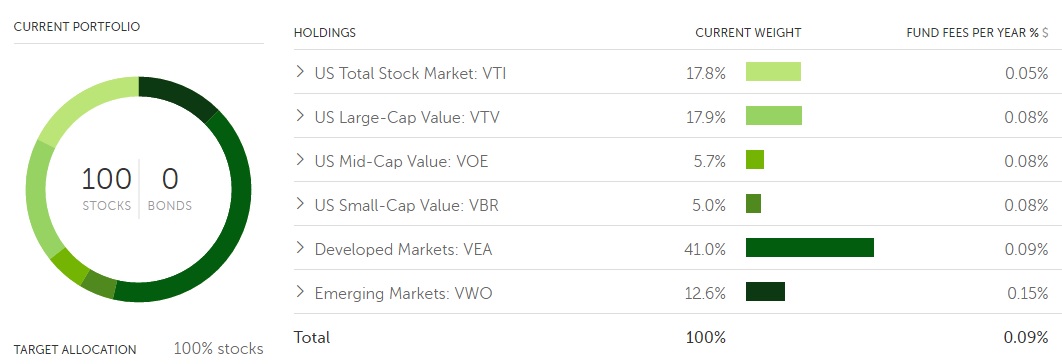

Without Betterment you would need to invest in Vanguard mutual funds directly, which you need $3,000 to start in each fund. With a 100% stock allocation you would need $18,000 to invest in 6 different funds, and they would all have an equal distribution of 16.6% each. Betterment has painstakingly evaluated the best allocation between these 6 funds to have and some are as low as 5% and some as high as 41%. Because different funds have different risks, by having a mixture of several funds, investing through Betterment lowers your overall risk and gives an opportunity for higher returns than having just an S+P 500 index fund.

If you go with Betterment the only decision you have to make is your stock to bond allocation, and Betterment will give you a recommendation based on your risk tolerance and time horizon. I would set this somewhere between 70% stocks and 100% stocks. This is a relatively minor decision in the big scheme of things. Currently I am invested 100% in stocks. Here is a snapshot of what a 100% stock Betterment account looks like:

Don’t Worry About Investment Returns

The bottom line is investment returns don’t matter until you have a substantial amount of savings. The difference between a 6% and an 8% return on $10,000 is only $200. Until you’ve broken into 6 figures the returns are largely inconsequential. Focus on increasing your savings rate and stacking your cash. Once you are over halfway to financial independence, then start to concern yourself more with returns, but until then, its mostly a waste of your time.

What have you done to increase your savings rate lately?

Leave a Reply