Why You Need Multi-Family Rentals In Retirement

It’s no secret I’m a big fan of real estate investing. I currently own 6 houses and plan to keep buying at a rate of 2 to 4 per year. Investors and authors routinely talk about using real estate to retire early, but not a lot is written about transitioning to real estate once you retire if you have not invested in real estate already. Rental real estate should be part of your retirement portfolio, and more specifically you need multi-family rentals in retirement. I currently don’t own any multifamily housing, however there is a strong argument for owning multi-family housing in retirement that I would like to talk about here. I plan to buy multi-family properties after we hit our goal of 10 single family houses.

Multi-Family Rentals Are More Efficient Than Single Family Rentals:

I currently have all my single family homes spread out over a city, with the furthest apart ones being about a 10 minute drive. This isn’t horrible, but it’s not ideal. With a large multi-family property you only have 1 location to worry about, 1 roof, 1 major set of appliances, 1 main sewer drain, etc. There is a lot of efficiency gained in this scale. You also gain efficiencies on making deals and financing. It’s 1 deal, not 20. It’s 1 loan with 1 set of closing costs, not 20. I pay around $3,000 in closing costs for a loan on a single family house, multiplied by 20 houses is $60,000, whereas 1 large apartment building might have $20,000 in closing costs, but no where near $60,000. It’s much easier to standardize materials when you have all your units in 1 building. It’s the same front door for every unit. The same windows, the same countertops, etc. This efficiency allows you (or your property manager at your request) to buy supplies in bulk and to save more money.

It’s also easier for a property manager to handle when all the units are in 1 location. You can typically get a better deal on management for a 20 unit apartment than you can for 20 single family homes spread out across the city. With a good property manager you have 1 point of contact, and have 1 major line item on your accounting every month. The management company handles everything and sends you a check every month. It’s vital to find the right property manager. Someone who treats people well and will manage your asset properly. Take your time to interview several to make sure you have the right company. Interview other property owners who use them and find out what they think. Interview the tenants in the buildings they manage to see what they think. Having multi-family rentals in retirement has clear advantages over single family homes. I highly recommend checking out the book How to Create Wealth Investing in Real Estate by Grant Cardone to learn more about multi-family investing.

Using Leverage With Multi-Family Rentals In Retirement:

At a minimum any real estate purchased should be at 75% loan to value. This means if you are buying a $1 million property your investment down payment would be $250,000. For a $250,000 buy in you are controlling a million dollar asset and its cash flow. If it returns a 5% cash flow after financing, that would be $50,000 you receive off of that $250,000. With only using a stock/bond 401K portfolio you do not benefit from this leverage. If your stocks returned 5%, this would be only $12,500 of cash flow. Having multi-family rentals in retirement has a massive cash flow advantage over following the 4% or 5% withdrawal rule for investment accounts.

Inflation Protection With Multi-Family Rentals In Retirement:

Inflation is guaranteed to happen and an increase in the rate of inflation is a very real possibility. We have had low inflation for the last 20 years, but our government and federal reserve have made it clear they plan on running the printing presses as fast as possible. Real estate, especially low to moderate income housing, will be an excellent hedge against inflation. Owning real estate is the best inflation hedge of any asset class because you already purchased the real asset, the mortgage on it is a fixed price based on pre-inflation dollars, the rental income is based on current dollars so it will increase with the inflation, and it is leveraged to 75% LTV meaning your pre-inflation cash bought 4X the assets that it otherwise could have done. If inflation increases at 3% per year it only takes 24 years for the rents to double.

According to MIT’s Economics department the value of Apartment buildings has a 98% correlation with CPI, meaning the value moves in lockstep with inflation. Income from apartments moves at 56% of CPI, which is still a very substantial hedge. Owning multi-family rentals in retirement is the best way to preserve capital and cash flow in an inflating economy.

Recession Protection With Multi-Family Rentals In Retirement:

Housing is a fixed need. If you are invested in affordable housing even during a global recession chances are you will do well. While other asset classes may fall 50% in value and cut dividend payments entirely, your rental properties will continue to produce income. People always need a place to live. When people lose their homes or need to downsize during a recession, they will become new customers for the affordable housing rental market, offsetting any current tenants who end up leaving because they can’t afford the rent. Vacancies will most likely not spike up and rents will most likely not drop during a recession.

In the 25 year period from 1992 to 2017 Multi-family housing had the highest return of any real estate sector with the second least volatility, with a 9.75% average return and a standard deviation of 7.75%. Standard deviation is a measurement for volatility in an asset, the higher the number the more volatility. For contrast the S+P 500 standard deviation is about 15%. This 25 year period included 2 major recessions, of course including the 2008 financial crash.

We are currently living in a microcosm with eviction moratoriums, but that will not last. Also the vast majority of tenants are still paying their rent.

Value Real Estate:

This type of real estate is extremely value oriented. Entry level low cost to affordable housing in the Midwest is an excellent value real estate segment. For the cost of a median house in silicon valley (around $1.5 million) you can get 30 units that cash flow $75,000 to $150,000 a year! These are considered Class B and Class C properties. Class A properties have been over built and represent the vast majority of new construction apartments over the last 20 years, while B and C have been substantially under built. There are more people that can afford these classes of rental apartments and they have much lower vacancy rates than Class A properties.

Furthermore we have several demographic trends that bode well for Class B Apartments in the Midwest.

We have the Covid-19 pandemic making it clear than a large set of jobs can be done remotely from any where in the world. For people who have been paying $4,000 to rent a studio in Silicon Valley, once remote work is fully greenlit for the long term we will see a migration to extraordinarily inexpensive places to live, like $800 2 bedroom apartments in Michigan, Ohio, and Indiana. This would be a great living option for remote workers who have large student loan debts to pay down.

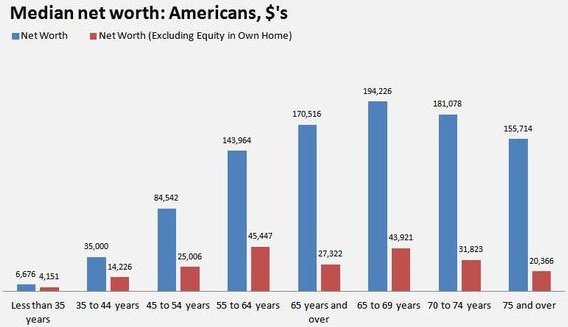

We have the entire baby boomer generation reaching retirement age with very little in savings at the median level and the vast majority of their wealth is in home equity. These boomers will be inclined to sell their homes to access their wealth and rent apartments, further reducing their expenses and maintenance costs. The median household headed by someone between the ages of 55 and 64 has $143,964 in total net worth and only $45,447 of that is outside of home equity. With this being the median that means 50% have less than this. $45,447 in total retirement assets would allow for a withdrawal of only $190 per month. These people will be mostly living off of Social Security in retirement.

We also have millennials and Gen Z waiting longer to buy houses than previous generations. This is for several reasons, with the highest being financial difficulties caused by entering the work force during the great recession saddled with tens to hundreds of thousands of dollars in student loan debt that was marketed by teachers, parents, and society as the only way to a bright financial future.

Affordable apartment rentals ranging from $600 per month to $900 per month are an excellent investment that will continue to have significant demand in the future in both good and bad economic conditions.

Tax Advantages From Multi-Family Rentals:

Real estate income is taxed as ordinary income, exactly as your 401K withdrawal will be taxed. Your real estate earnings in most scenarios will not be subject to self employment tax. Furthermore you may be able to claim the 20% QBI tax deduction depending on the situation.

All expenses on the property itself are deductible, either in the year the expenses occur or over a period of time through depreciation. Depreciation is the golden goose of tax breaks for rental properties. Your property management expense is also deductible. This is huge when you think about it. If your gross rents are $192,000 for the year and you pay 10% for property management, that’s $19,200. Since it is tax deductible and assuming you are in a combined state and federal tax bracket of 25%, you are effectively only paying $14,400 for someone else to handle all the headaches of a 20 unit building.

You can take depreciation on the whole building, even though you have a loan on it and the building is increasing in value every year. The land is the only part of the property you can not take depreciation on. If we assume the land is fairly cheap, lets say its valued at $10,000, The depreciation on a $990,000 building is $36,000 per year.

If the net income on the building was $50,000 before taking depreciation, only $14,000 of that cash income is actually taxed. This is a major advantage over a 401K draw, where everything will be taxed. This becomes even more stark as you magnify it.

- 2 20 units at $1M each with $250K down each would be $100,000 of cashflow taxed on $28,000. Compared to $500,000 of investment income at 5% would be $25,000 with $25,000 taxed.

- 4 20 units at $1M each with $250K down each would be $200,000 of cash flow taxed on $56,000. Compared to $1 million of investment income at 5% would be $50,000 with $50,000 taxed.

- 8 20 units at $1M each with $250K down each would be $400,000 of cash flow taxed on $112,000. Compared to $2 million of investment income at 10% would be $100,000 with $100,000 taxed.

Taking it a step further and applying the pass through QBI deduction of 20% would result in only having $11,200 of income taxed.

- 2 20 units at $1M each with $250K down each would be $100,000 of cashflow taxed on $22,400. Compared to $500,000 of investment income at 5% would be $25,000 with $25,000 taxed.

- 4 20 units at $1M each with $250K down each would be $200,000 of cash flow taxed on $44,800. Compared to $1 million of investment income at 5% would be $50,000 with $50,000 taxed.

- 8 20 units at $1M each with $250K down each would be $400,000 of cash flow taxed on $89,600. Compared to $2 million of investment income at 10% would be $100,000 with $100,000 taxed.

Appreciation From Multi-Family Rentals:

Real estate values tend to go up over time. Once again, leverage helps here. If a $1 million asset is appreciating at 4% per year in value, that’s $40,000 in increase per year, the equivalent of the same $250,000 in a brokerage account appreciating at 16%. This is over and above the income being earned by the property.

With multi family properties containing more than 4 units the value of the property is based off of cash flow. This gives a smart owner the ability to force appreciation through improvements in cash flow. As an example, lets say we are dealing with a 20 unit building that currently generates $50,000 per year in cash flow, or $2,500 per unit per year, the same as $208 per unit per month. The units rent for $800 per month. The property is trading at around 10X Net Operating Income, that means every dollar of cash flow improvement you make gives an automatic 10X return.

If you can increase rents by $25 per unit per month that’s $6,000 in more cash flow. Because it adds 10X to the value of the building, the building is now worth $60,000 more. You may be able to do this to catch up to market rates for an under performing property, or by making some value improvements for the tenants. If tenants are paying below market rate rent, they most likely won’t leave because of this increase because they can not find a better deal elsewhere.

If you file an appeal on your property taxes and get your yearly taxes reduced by $2,000 you added $20,000 in value to the building.

If you switch property managers and get a reduction from 10% of gross rents to 8% of gross rents due to the volume discount you dropped the expense from $19,200 to $15,840 (based on new rents). That’s $3,360. You added another $33,600 in value.

You pay a plumber a 1 time fee to come through and fix leaks in all the units. It cost $1,000 for the plumber, but saved $3,000 a year, every year, on your water/sewer bill. That’s another $30,000 in value.

You go with a higher deductible on your insurance and pay in full for the year, cutting your insurance cost by $2,000 per year, adding $20,000 in value.

Now your property instead of cash flowing $50,000 is cash flowing $66,360 and is worth $1,163,600.

Cash out Refinance:

You can cash out refinance a rental property to retrieve some of your equity. If you took all the actions above and increased the buildings cashflow by $16,360 per year then the bank would see it as being worth $1,163,600. A loan at 75% LTV would be $872,700. You could refinance the building, take $122,000 of cash back and have only $128,000 of cash in the property, yet still be cash flowing over $60,000 per year. You still have almost $300,000 of equity in the building but your cash if freed up for other investments, including your next apartment building. The loan proceeds from the cash out is tax free cash to you, to either add to your bank account or reinvest in your next property.

Additional Added Value With Multi-Family Properties:

When you are the owner you can make decisions about your property that can greatly increase its income. All those above tweaks resulting in a massive increase in income and value, but there is still more you can do. Several of these ideas are the same concepts that work well if you are investing in a mobile home park. Check out the book Multi-Family Millions: How Anyone Can Reposition Apartments for Big Profits to learn more methods to increase the value of multi-family properties.

- Adding storage: Adding storage is a big value add for a multi-family property. If the property is on a large piece of land you can build an onsite storage facility. Alternatively you can take a section of the basement and convert it into several storage units and offer to rent those out to tenants. Experiment with the pricing, starting high until you get all the units fully rented.

- Adding vending machines: How often do you think your residents run to the corner store for something small? Having vending machines with basic drinks and snacks is a great idea, but I think you should go a step further and have OTC drugs, non perishable quick meals, and general hygiene products in your machines. You don’t have to operate these yourself. You can have this be a responsibility of your property manager for a cut of the proceeds or have an independent vending company do all the work and give you a percentage. Make sure you have laundry detergent in one of them.

- Adding laundry machines: The laundry machines are huge if the individual units don’t have individual hookups. It’s a big convenience add for the tenants to not have to go to the laundry mat and you get some extra revenue. I came across a post on Bigger Pockets by someone who had an apartment complex with 10 coin op washers and dryers, he said “For 120 units I would take 3600 to 4000 a month to the bank in quarters.. HEAVY..” For a 20 unit building this would scale down to $600 to $667 per month! These also don’t have to be serviced by you. You can get a service agreement with an outside company and if a repair is needed your property manager calls them and they handle it.

- Adding advertising: Adding advertising to your property may be possible. The side of your building could be a good canvas, or you could build a billboard facing a busy street. These actions would of course need local government approval.

- Adding Solar Panels: When I did the math for installing solar panels on my house (with battery backup) the effective return on investment was around 10% (after tax credits). If the numbers held true for the apartment as a whole, then this could be a big opportunity to earn more money off the same building. If you finance the panel installation to 75% LTV and get a 10% return, your cash on cash return is really 40%. Another major bonus is that currently Solar panels can be depreciated in 5 years, even though the life expectancy is closer to 40 years. This is a major tax advantage.

- Get a RUBS system installed: RUBS is a ratio utility billing system. Effectively its a way to meter all the units that share a common source, be it gas, electricity, or water. This is a way to bill the utilities to the tenants without having 20 completely separate systems. If some of these utilities are already included in the rent, modify the leases going forward to provide X units or a fixed dollar amount credit for the utility. People who conserve may actually come out ahead and those who don’t will pay for their usage, which will ultimately drop your costs as the operator. RUBS system tend to save the operator 25% on utility costs.

Seller Financing Multi-Family Rentals In Retirement:

Often these large multi family properties are sold using seller financing. This allows the buyer to sidestep the bank and receive some favorable terms the bank may not be willing to offer. Not only that, but these properties have oftentimes been sold numerous times with seller financing, providing someone in a strong financial position the ability to reduce his or her purchase price after the deal is done.

Here’s an example:

Step 1:

In 2005 Bob Sold the property for $600,000 to Steve on a 20 year seller financed loan of $500,000.

Step 2:

In 2010 Steve sold the property to Scott for $700,000. At the time Steve still owed $400,000 on the original loan. Scott agreed to assume the remainder of Scott’s loan, give a $100,000 down payment, and write a new loan to Steve for the $200,000 difference.

Step 3:

In 2015 Scott sells the property to Katrina for $800,000. She assumes the 2 seller financed loans now at $300,000 and $150,000, she pays $100,000 down and writes a new seller financed loan to Scott for the $350,000 difference.

Step 4:

Now in 2020 Katrina wants to sell the property to you for $900,000. It has the following loans due:

- $200,000 to Bob

- $100,000 to Steve

- $300,000 to Scott

- You assume the loans, give her a $100,000 down payment, and she agrees to seller finance $200,000 at 5%.

Step 5:

Now you get to work. You paid $900,000 for the building, but you may be able to get it for less. Here’s how. After you closed with Katrina you do your research on Bob, Steve, and Scott. Their lives may have changed dramatically since they sold the property. Find out everything you can. Where they work, what’s going on in their lives, etc. Write them a letter offering to purchase the debt back from them at a reduced price. Essentially you will make yourself the JG Wentworth here. If they are interested in selling their debt payments for a large lump sum it would be more valuable to you than to any other debt buyer.

Bob may need cash for his retirement and he’s uneasy about the loan because its been resold so many times. He’s already received more than his original investment back and just wants to clean his hands of the whole thing. He might cut a deal for 60 cents on the dollar. You pay him $120,000 and the debt is cleared. You saved $80,000.

Steve’s OK with the loan structure and doesn’t want to sell. He says his daughter starts college next year and that he will contact you if he’s interested. Continue to write him a letter every 6 months.

Scott has hit hard times. His house was foreclosed on, he’s facing bankruptcy, and his son was charged with a serious crime that he’s forking over all his cash to lawyers to keep him from going to prison. Scott really needs money and he’s willing to sell his loan at 50 cents on the dollar. You pay him $150,000 and you saved $150,000.

By negotiating this debt you dropped your cost in the property down $230,000. Keep in contact with both Steve and Katrina and they may come to a point where they need a lump sum more than the cash flow. Steve’s daughter is going to college and most likely those bills will pile up and your solution of buying his debt may be a great deal for him. Check out the book

Investing in Fixer-Uppers : A Complete Guide to Buying Low, Fixing Smart, Adding Value, and Selling (or Renting) High for more information on this strategy.

Build Generational Wealth With Multi-Family Rentals In Retirement:

Multifamily properties are a great way to build generational wealth and have distinct tax advantages over 401K/IRA plans. You can’t transfer ownership of your retirement account directly. In order to transfer ownership of any assets in your retirement account on an ongoing basis you must create a taxable event. You have to withdrawal the money from your retirement account, which you will incur tax on. Then you can give away that money, up to the $15,000 per person per year maximum without using up your lifetime exclusion on the estate tax. With real estate outside of retirement accounts this isn’t the case.

Although you purchased the property with leverage, over time it will pay itself off. On 30 year loans, these properties will each build $15,000 in equity the first year and increase every year, not including appreciation. The tenants pay off the properties for you.

Giving An Inheritance At Death:

Under current laws when someone passes away the heirs receive a stepped up basis. If you bought one of these apartments buildings for $1 million and it increases to $2 million in value, your child will receive the asset with a basis of $2 million, meaning that if he chooses to sell it, no capital gains tax would be owed. The depreciation recapture also goes away because your son didn’t depreciate it. So that $36,000 a year for 27.5 years you received doesn’t have to be repaid when your son sells it for $2 million. Your son can use the new stepped up basis to start his own 27.5 year depreciation on the property if he chooses to keep it. This is a major advantage of investing in real estate and never selling it.

Giving An Inheritance While Living, In an LLC:

If an apartment building is held in an LLC, you can give away shares in the LLC to your children or grandchildren at present value, up to that $15,000 per person per year. Consult a tax attorney for this setup. Since you can do this in an ongoing fashion every year, you not only transfer ownership of the assets without incurring any debt or tax liabilities, you also start syphoning off some income to your children during this time. If say over the first 10 years you transfer 25% of the ownership to your children and the LLC has $100,000 of income, $75,000 would stay with you and $25,000 would go to the children.

Another trick with this method is that the shares going to the the children and grandchildren can be discounted because they are not given voting rights and because they can’t sell their shares on the open market. So if the total value of the LLC is $1 million rather than giving 1.5% per year to each person at a face value of $15,000 you could give them closer to 2.5% per year or $25,000.

This strategy kills 4 birds with 1 stone. It transfers assets to your heirs avoiding the estate tax. It gives away assets before they appreciate, allowing your children and grandchildren to receive asset appreciation early on and further reduce your future taxable estate. It transfers income to your children and grandchildren to give them passive income now (which they can re-invest into their own retirement accounts or rental properties), and it reduces your taxable income in the highest bracket for the year.

I would caution to keep each apartment building in its own LLC as you scale. This is to limit the reach of creditors in the event of a lawsuit. If you have 5 apartment buildings in 1 LLC, and someone breaks a leg on the sidewalk in front of 1 of the buildings and wins a lawsuit against the LLC, they could take all 5 buildings. If each building is in its own LLC only that one building is at risk.

The aspect of lowering your estate before you die is extremely important. Right now the estate tax kicks in at $11.58 million per person, so $23.16 million for a couple. Less than 1% of people currently have enough assets to worry about this, but it very easily could be you. For people who are actively trying to build their net worth and are buying apartment buildings the odds are higher that they will reach this threshold. The Estate tax accelerates very quickly to 40% of assets. If you and your wife have $100 million at death, the estate tax could cost you $30 million! The estate tax also could change at any time by the whims of congress. In the last 20 years the estate tax has varied from being completely non existent in 2010 and the current level of an $11.58 million exemption followed by a 40% rate, to a high of only a $625,000 exemption and a 55% top rate. The estate tax laws will change substantially over the next 50 years, so transfer assets while you can!

Getting Started:

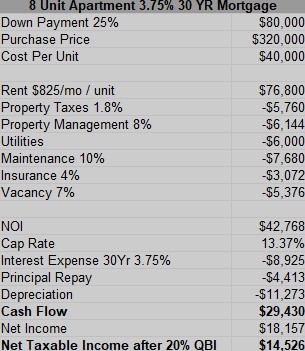

You have to keep an eye out for deals, but in the Midwest I can routinely find properties at around $40,000 per unit. This is on the lower end and $50,000 to $60,000 is more typical. You want to be looking for a deal and negotiate very strongly when buying. As with any real estate transaction the buy is where you really make the money. At $40,000 per unit an 8 unit property would then cost around $320,000 with $80,000 needed for a down payment, provided you are getting bank financing. If seller financed you may be able to get a much smaller down payment. Everything is negotiable. If you have a smaller down payment the seller will most likely want a higher interest rate and/or a shorter term.

Using all the details we have in the earlier examples, if we got the same building at $40,000 per unit instead of $50,000 a unit our numbers would look like this.

For someone with a relatively small nest egg of $300,000, an $80,000 down payment should be feasible. You don’t have to be super rich to invest in multifamily real estate. $80,000 isn’t a small chunk of change by any means, but to be able to leverage it into 8 rental units may be an excellent deal and a great way to increase cash flow. Even for someone with substantially more resources starting small with an 8 or 10 unit building is a great way to get started in multi-family investing.

Example:

For most retirees that have invested diligently over the years this should not be a problem to come up with. Let’s look at a couple who both earned an average of $50,000 per year and saved 15% of their income per year, with an employer match of 5%. This works out to $20,000 per year of savings. Invested from age 35 to 65 at 8% returns they would have $2.5 million.

I would recommend them investing at least 25% of their retirement savings in multifamily real estate. This would be around $625,000. That $625,000 would be down payments for a total of $2.5 million in real estate, allowing them to buy 60 units at $40,000 per unit.

Using the numbers we did above with a 20 unit building generating $50,000, they could buy 3 of these for 2.4 million (saving $500,000 over our example at 50K/unit). They would receive $150,000 of income from these properties off of $600,000 in cash.

Using the 5% withdrawal rate on their remaining 401K they would have an income of $93,750 from this, for a combined income of $243,750! This couple would also be able to receive Social Security benefits of about $1,400 a month each, or a combined total of $33,600 per year. I think an annual income of $277,000 is pretty darn good!

The multi-family rental building is providing: $50,000 in cashflow, $15,000 in debt repayment, and $40,000 in appreciation every year, while only being taxes at $22,400. And this isn’t including any value add strategies!

Precautions And Limitations:

Liability Risk: I discussed putting these properties into an LLC. I’ve made it clear on this blog that I use umbrella insurance for my properties currently and they are all in my name. I plan to continue with that at least until I get to 10 properties. At a certain point, umbrella insurance is not enough. When you have dozens to hundreds of units you need more protection. An LLC is a good start, but it is also imperative to have excellent insurance coverage inside that LLC to protect its assets. This should include several million dollars in liability insurance. Each building should also be in its own LLC.

Property Management Risk: This isn’t truly 100% passive. You have to spend some time watching the watcher. If you are asleep at the wheel a bad property manager could be charging well below market rent to keep the turnover low and the complaints low. People who know they are paying below market rent will not make a fuss and they won’t move out. A bad property manager will also charge you double the price for materials and $100 an hour for a repairman they are paying $15 an hour for, while charging 3 hours for a 15 minute job. Even worse, a property manager who does not follow the law can get you in legal trouble. There have been property managers who have illegally discriminated based on religion, family status, race, and disability. These managers open up an insane amount of liability to the company. You need to vet these people and keep an eye on them.

Competition: Competition exists, but is much more limited than you might think. Of all the 210 million+ adults in the United States only about 8 million are real estate investors. Of those, only 20% own more than 10 units, so the entire competition is only 1.6 million people across the entire country. I believe the next 2 years will be an amazing time to buy multi-family properties. Interest rates will be at historic lows, many investors will be getting out, both due to a demographic shift of aging baby boomers wanting out of the business and to marginal players exiting due to the short term constraints caused by Covid-19. To beat out the competition, check out the books Make Money with Small Income Properties and The Infinite Game

.

Real Multi-Family Properties For Sale:

Here are some actual listings available right now.

This 18 unit building in Dayton, OH is only $720,000 with rent rolls of $11,000 per month.

This 22 unit complex in Stanton, KY, is $765,000.

This 24 unit building in Shoals, IN is $864,000.

This 22 unit is Monticello, IN for $849,000 is LAKE FRONT! Walking distance to the Indiana Beach theme park. This is an amazing property.

This 10 unit property in Antwerp, OH is $399,000 with a 10% Cap rate.

This 16 unit property in Rockville, IN is $360,000. (All 1 bed 1 bath).

This 6 unit in Dayton, OH is $249,000 with $43,800 in gross rents!

Deals are out there. The numbers I’ve used in this article are not pie in the sky. These are realist numbers that you can achieve, and most likely out perform. These listings are of course, also negotiable. Some have already cut the prices and others have been on the market for a long time. It’s possible to get even better prices than this.

What do you think about investing in multi-family rentals in retirement? Are you planning to add them to your portfolio? If you own an apartment building please share your knowledge and let me know what I’m missing!

Leave a Reply