Systemic Changes To Address Racial Inequality – Part 4: Government Assistance

Our government does a lot of social engineering through the tax code and through our safety net programs. These programs and the tax code sometimes contain incentives that trap people in poverty and create a culture of dependence. These incentives have destroyed families and caused generations of poverty, not alleviated it. Our programs should be focused on increased freedom and increased wealth building. A lack of wealth and resources is at the root of the problems we are facing.

Government Assistance And Tax Credits To Address Racial Inequality:

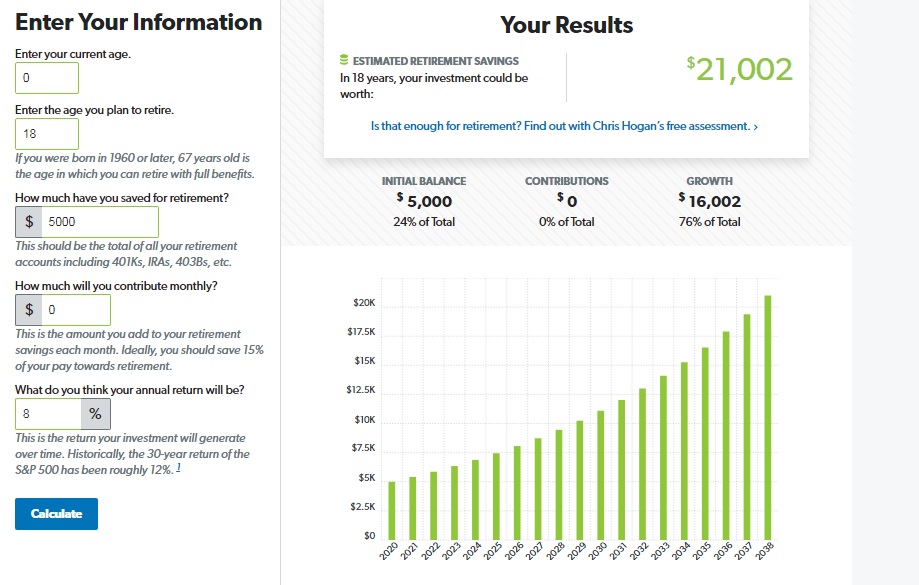

Baby Stocks: $5,000 at Birth: My first proposal to government assistance will perhaps make the largest dent in the wealth gap. This proposal is similar to the Baby bonds proposal introduced by Senator Corey Booker, but using the stock market for higher returns. Compounding interest is the best way to build long term wealth and the easiest intervention is at birth, because this gives the most time for the money to grow. 18 years is a long enough window that a total stock market index fund makes a lot more sense than bonds. We have about 3.8 million births per year in this country. 3.8 million births X $1,000 is 3.8 billion. X 5 is $19 Billion per year. pocket change for our country. If we can spend close to $1 trillion a year on military spending, we can spend $20 billion on investing in our citizens early on. This early intervention is the most bang for your tax dollars we can get. I decided that this would be a great way to go as a national program when I researched building generational wealth and decided one of the items on that list would be a large gift in an investment account to my grandchildren at their birth, the math just works well.

As a way to reduce costs we could even have an adjustment here where a phaseout begins for families at 300% of FPL and drops it to a floor of 25% of the total credit for families at 500% of FPL or above. This could cut the total yearly cost to under $15 billion.

Corey Booker’s plan, which is a bit more complicated and has yearly contributions based on family income shows that by JUST doing this would increase the median wealth among young Black Americans from $2,900 to $57,845, and for young White Americans from $46,000 to $79,159. Instead of White Americans having 16 times the wealth of Black Americans, this would drop to under 1.5X.

This $19 Billion a year plan is 1/3 the cost of Corey Booker’s plan, but the median result is about the same due to funding more money earlier and to stock market returns of 8% over government bond returns of 3% or less. Don’t get me wrong, I am not opposed to Corey Booker’s plan, I just think this is a better overall solution. Alternatively it could follow his plan 100%, with the parent being able to choose between an all bond, an all stock, and a “target retirement date” mixed fund. ANY steps towards some sort of gift at birth for children of this country is a step in the right direction.

$5,000 invested at 8% will be $21,000 at 18. This money would NOT count as assets against any means tested programs. Starting out with roughly $21,000 will give every child a major leg up in launching in life. This is an emergency fund, education expenses, retirement savings, or business and investing seed money. This step alone can solve a major part of the wealth gap.

My parents paid $13,000 for my college costs (over a 8 year period of time, I was slow being a young parent and working full time or close to full time through it.), $2,000 in down payment assistance for our first home out of the $10,000 we needed to move in, and roughly $3,000 for a car they let me drive that they eventually signed over to me. This roughly $20,000 in help I received as a White child of fiscally well off parents helped substantially in me becoming wealthy. If every kid had the same start I did, then we could close a big portion of this gap.

Changing the Current Government Assistance Programs: Current government assistance programs have several problems. They cause the breakdown of the family, they make work have a negative return, they discourage saving and investing, and they create a giant confusing bureaucracy with a massive amount of government control.

Breakdown of Family: Our welfare system is set up in a way that traps people and destroys families. Our system economically requires the breakdown of family. In 1940 only 13.6% of Black children lived in a home without their father, today it is 65%. (For White families it is 24%.) This is most likely one of the largest demographic changes in household composition in history, outside of slavery and genocides.

Married couples, especially low income married couples with children face an extremely high negative tax rate compared to being separated. Responding to economic incentives, being married, and fathers even living in the home doesn’t make sense. You lose massive amounts of income to be together. These short term incentives prevent long term wealth from being created from 2 parents working together to build wealth and raise their children.

Here’s an example just based on the Earned Income Credit. A mom with 3 children earns $20,000 per year. She would receive $6,347. If she married a man who earned the same amount as her, this would drop to $3,354. Food stamps and housing assistance would also be cut.

Children who grow up without a father in the home are more likely to drop out of school, go to jail, live in poverty as adults, and have children out of wedlock. This then causes the cycle to repeat. The incentives that encourage fatherless homes are a major culprit in the extreme barriers to economic mobility for people of color and for poor White families. When you couple the welfare incentives with the mass incarceration of primarily Black men no wonder we have such a low rate of Black fathers in the home.

The overall decline in marriage rates over the past 70 years has disproportionately affected lower income people. For Americans between 18 and 55, 26% of poor people are married, 39% of working class are married, and 56% of middle and upper class are married. This closely follows the tax code. Marriage is a penalty for lower income people and is rewarded for higher income people in our tax code.

Disincentive to Work: work is disencitivized with several major drop off cliffs that sometimes carry tax rates of several thousand percent. A single mom may not see any increase in standard of living and in fact will be faced with several decreases in economic earning moving from $25,000 a year in income to $50,000 a year in income. Remember the comparison isn’t jumping from a $25,000 a year job to a $50,000 a year job, it’s moving up $2,000 to $5,000 a year, and doing so will result in several years where working more hours, increasing education, and taking on leadership roles will actually cause her standard of living to fall! For most, there is no light at the end of the tunnel.

Disincentive to Save: For food stamps, housing assistance and other programs there are asset tests that vary by state. These asset tests prevent people from saving money. Depending on the state, if you have $2,000 in assets you can lose $7,000+ in yearly income. Facing these incentives would you keep an emergency fund, which is the first major stepping stone out of poverty?

Winner Take All In Housing: For the Section 8 program there are way more people that need housing assistance than there is budgeting for it. Section 8 vouchers are awarded on a first come first serve basis. In most cities there is a multiple year waiting list, and most wait lists are closed to new applicants. Once people get on Section 8 there is a strong incentive to never lose it. If 10 people qualify for the help, most likely only 1 is getting it, and that 1 is having greater than half his or her rent covered for several years. The average voucher recipient stays on Section 8 for 6.6 years. On the flip side of this government regulations cause fewer landlords to accept Section 8 which can trap people from being able to move. Because Section 8 amounts are determined by very wide geographical areas, Section 8 voucher holders are most likely to only find places to rent in the lower valued neighborhoods. There are a lot of other issues with this program that I will tackle in another article.

Giant Bureaucracy and Government Control: The bureaucracy of administration of these programs is intense. They employ thousands of people and make people jump through an insane amount of hoops, including reporting all their income and assets. I don’t think that our government should know what assets you have and who is living in your home.

This bureaucracy has a tie in to criminal justice. This system is also used as part of mass incarceration. My Sister in law had a job once where she was working really long hours (12+ per day). She let her babysitter use her food stamps card to get food for her kids (the babysitter was a family friend). This was caught (someone noticed it and called a tip line) she had to go to court and almost went to jail. She had to pay steep fines and be on probation.

Solution: End all means tested programs and replace with a Universal Basic Income (UBI) of $800 a month per adult tied to CPI. This includes the earned income tax credit and the child tax credit. I originally was strongly opposed to a UBI, however when I realized all of the bad government incentives we can get rid of and how much more equitable the system would be than our current system, I started becoming a supporter of it.

This does the following:

- Removes the disincentive to work: Now work has the exact same tax rates for everyone. No cliffs to fall off of. Working extra lets you keep most of your money. It is always better to work more.

- Removes the disincentive to save: With a UBI you aren’t penalized for saving money.

- Removes the incentive of single motherhood: Now a dual parent household makes sense. In addition to another adult bringing in $9,600 a year from the UBI his income from work will not cause you to lose your apartment, food assistance, etc.

- Removes the bureaucracy: All that is needed is when people turn 18 to set up their account. No forms, no hoops, no asset / income reporting.

- Removes the leaches: Poor single moms have a target on their backs for manipulative loser men. These guys know she’s getting a big tax check etc, so they sweet talk her and do everything they can to mooch off her for a free place to live, free food, etc, but without contributing to the household. Worse, many of them become controlling and abusive, so in addition to mooching off her income to take care of her kids, they also add in domestic abuse. Of course moochers and losers will still exist, but their targets won’t exclusively be poor single moms. The UBI would also give these men a basic standard of living and make them able to see a path to be economically self reliant.

How do we pay for it?

With 210,000,000 US citizens over 18 the cost of this UBI would be right at $2 trillion. 1 Action is not going to pay for this. We need to make major changes to federal tax revenues and expenses to cover this cost. At freedom-dividend.com there is a breakdown of one method of making the numbers work for a $1,000 a month plan. I believe that a $800 a month plan will be just as effective and will cost 20% less. The plan at Freedom Dividend does not go as far as I would in providing funding. He does not fully eliminate all welfare programs including child tax credit and the EIC. He also does not advocate for cutting our military spending.

We remove the other programs. Earned income credit, the child tax credit, the mortgage interest deduction, food stamps, Section 8, cash assistance, daycare assistance. All of those go away. Then we cut our military spending in half and use that money because we spend more than the next 10 countries combined. (We actually spend more than the next 40 combined when you add in all our “Alphabet soup “defense” agencies.) Our lopsided “guns and butter equation” has destroyed our country financially and we see no benefit from the marginal expenditures. This is not radical. We are talking about scaling down our military spending to year 2000 levels, and we would still be spending more than the next 2 countries combined. In cooperation with these actions we need to push other NATO countries to cover the cost of their own defense.

Replacing the current welfare system accounts for about $600 Billion of the cost. The mortgage interest tax deduction, child tax credit, and EIC add in another roughly $200 Billion. The economic growth caused by the UBI will bring in another $550 Billion. The stepped up income tax on income that is now in a higher tax bracket will add another $250 Billion. This adds up to $1.6 trillion that is revenue neutral. Lowering current military spending to year 2000 levels adds another $400 Billion of the cost, putting us at $2 trillion without increasing taxes. Additionally every year Americans could choose to “opt out” for the year and return the money to the treasury. Many high earner and high net worth people would choose to do so, if for nothing else, for political reasons. If 10% of the population opted out it would reduce the cost by $200 Billion. Even if we had to increase tax rates to pay for this, I think it makes sense. The negative effects of our current welfare systems are too detrimental to our society to keep them in place.

Opponents to the UBI have said that the UBI will result in fewer people working and cause a net loss in GDP. I strongly believe that the opposite is true. The number one rule of economics is that people respond to incentives. For the past 6 decades we have had incentives in place to keep people from earning more money. With the UBI we can get rid of those incentives and people will not be penalized for working and earning more. “Go as far as you can see, when you get there, you will be able to see further” More people will start businesses, more people will work, and the standard of living for all our citizens will greatly improve. For more on how a UBI may look, check out the book: Give People Money: How a Universal Basic Income Would End Poverty, Revolutionize Work, and Remake the World.

Increased Marriage Rates: Since the UBI encourages dual earner households, then it stands to reason that marriage rates will increase. Wealth building is a team exercise. Now working together more people will be able to save money and buy homes. Marriage also brings long term protections including social security benefits, custody of children, workplace benefits, and automatic inheritance. With households composed of 2 working adults and most household costs being fixed, there is more discretionary money in the budget for saving and investing, as well as for buying more goods and services. The proportion of married families in poverty compared to non-married families in poverty is very stark. Just fixing this incentive will make a major change.

Actions You Can Take:

- Understand that the breakdown of family has been a product of government actions, not of cultural and individual actions and choices.

- Understand that our government supports high income housing much more than it supports low income housing.

- Contact your congressmen and senators to support a baby bonds/baby stock program. This should not be a partisan issue.

- Contact your congressmen and senators about a UBI. Continue to learn about how a UBI could work. Know that a UBI doesn’t necessarily mean massive increases in taxes and deficit spending. View it as a re-framing of our current social safety net programs.

- If you are financially stable and know a family that you think is trapped economically, consider starting an investment account for the children that you add to every month. Similar to a baby bonds program. Stockpile would be a great program for this. Although the child would be the owner of the account, since you are the custodian of the account the asset would not count against the parents for means tested programs and at 18 or 21 depending on your state would transfer to control of the child. Investing $10 per week for 18 years at 8% annualized growth will become $20,000! This amount of wealth would be a major help to launching into the world and to breaking the cycle of systemic poverty. Do this for your own children as well.

Continue to part 5: Housing

Leave a Reply