Quarter 4 2017 Update

2017 was our best year financially yet. Despite setbacks we hit a savings rate of 44%, not quite the 50% I wanted, but certainly close. We saved just under $40,000 this year. I think overall the targets I’ve been shooting for are a bit too lofty and I need to adjust my goals downward. Psychologically it’s much better to be surprised if you beat a goal, than to be frustrated that you miss an overzealous target. I was actually fairly frustrated when I realized we were coming in at under $40K this year in total savings, til I said it out loud to my wife what was bugging me. “We’re only on track to save $38,500 and we should have saved $40,000!” Wah. what a horrible problem to have lol.

Health:

Mrs. C. was diagnosed with Graves disease in January after being sick for multiple years. It generally takes over 3 years for auto immune disorders to get properly diagnosed. She had her thyroid killed with radiation in February, and although her worst problems are gone she still has issues from this and will need blood tests and medication for the rest of her life.

Our 9 year old had a second liver biopsy this year which came back much better than the one he had in 2016. His liver seems to have healed a lot of the damage. He still needs to do periodic blood work and another biopsy in 2018 or 2019 depending on the blood work for tracking purposes.

Our 14 year old has completed phase 1 of his braces! His teeth are WAY straighter already. The first phase widened his bite and started straightening his teeth. Phase 2 won’t start until all of his adult teeth are in, which shouldn’t be until sometime in 2019.

Needless to say, health care expenses were a really high spending category this year.

Spending:

Total yearly spending ended up at $48,411. This includes $3,000 for Phase 1 of my sons braces (complete), $3,500 for health care expenses, including Mrs. C’s thyroid ablation due to Graves disease which led us to not only hitting our deductible this year, but also our out of pocket max. We spent $400 on a vision therapy program for our 9 year old who needed convergence therapy. Total medical expenses accounted for 8% of our spending.

By the way these expenses would have been horrendous emergencies 7 years ago to us. Having an emergency fund and all our ducks in a row made money the least of our worries when dealing with these issues. When you don’t have any cash stashed every time it rains you are drowning. Having a fully funded emergency fund allows you to weather 95% of the storms this world can throw at you.

Our highest expenses for the year were groceries at $9,348 and housing at $8,940 (including property taxes and insurance). Our grocery bill is slightly inflated because it also includes household cleaners, pet supplies, and medications.

Fun:

People often seem to think that in order to hit a high savings rate you must live a life completely devoid of fun and you can’t spend any money. This is far from the truth.

We bought a telescope

Our summer vacation was a trip to Bowling Green, KY where my parents live. We visited Dinosaur World and the Corvette Museum. We also spent half a day at Mammoth National Park.

Our summer vacation was a trip to Bowling Green, KY where my parents live. We visited Dinosaur World and the Corvette Museum. We also spent half a day at Mammoth National Park.

At the beginning of the spring season I spent roughly $150 and built a rock climbing wall for the kids. We’ve got a lot of use out of this and it will last for many years.

I pre-ordered tickets for Mrs C. and I to take the two younger kids to watch Daniel Tiger live at our local performing arts center. I paid a premium to get us really good seats to ensure that the short dudes won’t have anyone blocking their view. This ran us $184.

We spent $300 on a membership to The Museum of Science and Industry in November and have already gotten our money’s worth. For a larger family memberships often make sense. We sprung for the Explorer level membership which is $95 more than the family membership. It allows 1 more guest and instead of slightly discounted tickets to special exhibits, films in the giant dome theater, and tours, it gives unlimited free tickets to all of those. At $12 a piece for adults and $9 a piece for kids for those extras, the Explorer level membership was a no brainer. The Museum is about an hour and a half from us, so it makes for a convenient day trip.

We spent $300 on a membership to The Museum of Science and Industry in November and have already gotten our money’s worth. For a larger family memberships often make sense. We sprung for the Explorer level membership which is $95 more than the family membership. It allows 1 more guest and instead of slightly discounted tickets to special exhibits, films in the giant dome theater, and tours, it gives unlimited free tickets to all of those. At $12 a piece for adults and $9 a piece for kids for those extras, the Explorer level membership was a no brainer. The Museum is about an hour and a half from us, so it makes for a convenient day trip.

Savings:

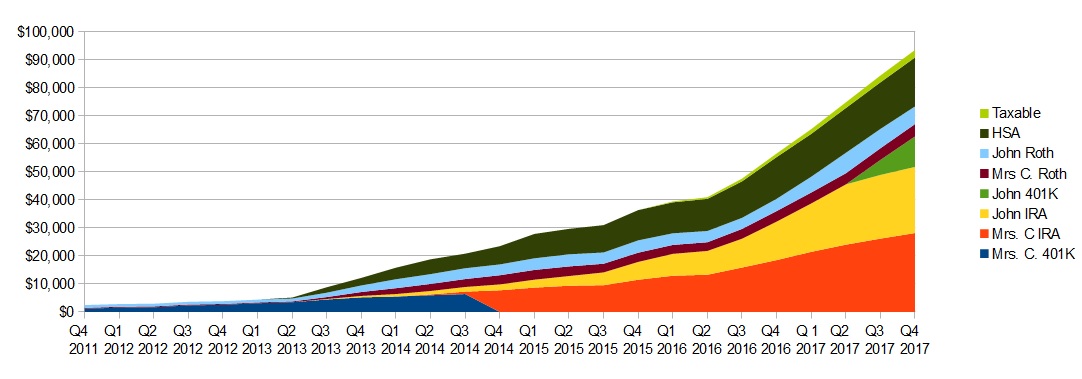

Our total savings for the year came in at $38,354. Here’s the breakdown:

- 401K: $10,428

- IRAs: $10,576

- Taxable brokerage: $1,000

- Extra On House: $13,000

- Increased Cash: $3,350

Saving a large portion of our income comes from 4 basic decisions:

1. Keeping house expenses low: Our total housing costs are only 10.3% of our net after tax income. This is 20% below most guidelines. Although a good deal of this percentage being as low as it is is due to increases in our income, when we bought the house it was still much cheaper than 30% of our income.

2. Keeping vehicle expenses down: We pay cash for our vehicles are drive very modest vehicles compared to our income and net worth. Our total vehicle value is only 8.8% of net income and only 2.8% of our net worth.

3. Optimizing taxes: I use my tax planning spreadsheet to optimize our taxes. We contribute a lot to tax deferred accounts, which is able to keep our AGI low. A low AGI means a lower tax bill, lower Obamacare health insurance premiums, and the ability to qualify for the retirement savers tax credit.

4. Bank raises: As our income has increased we have saved the vast majority of those increases.

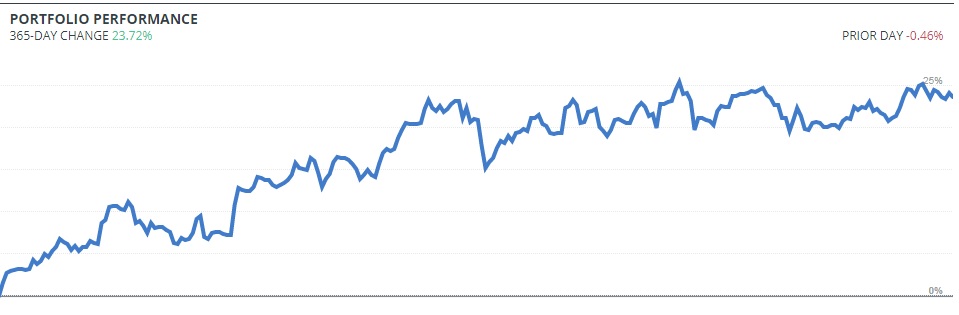

Investments:

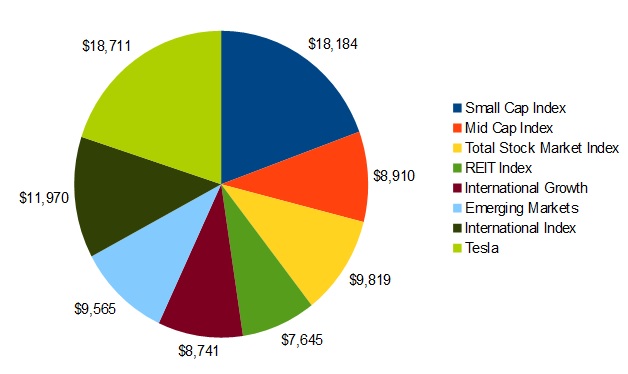

I track my investments with Personal Capital and using my own spreadsheets and charts. All of my accounts are linked to Personal Capital, so I can quickly see how I am doing overall without having to log in to a half dozen different accounts. For 2017 we had a total return of 23.72%.

- Small Cap Index: $18,184 19.42%

- Mid Cap Index $8,910 9.52%

- Total Stock Market Index/Lg Cap Index $9,819 10.49%

- REIT Index $7,645 8.17%

- International Growth Index $8,741 9.34%

- Emerging Markets Index $9,565 10.22%

- International Stock Index $11,970 12.79%

- Tesla $18,711 19.99%

- eBay $75 .08%

I stopped contributing to my taxable Betterment account in November. I’m happy with Betterment, but I feel like I am trying to do too many things. We are contributing around 25% of our income to retirement accounts and 20% of our income to paying off the house. We are contributing so much to our retirement accounts to keep us from falling off one of the Obamacare cliffs at 200% of FPL. If it weren’t for the Obamacare cliff I would reduce our retirement accounts and put more on paying off the house.

I stopped contributing to my taxable Betterment account in November. I’m happy with Betterment, but I feel like I am trying to do too many things. We are contributing around 25% of our income to retirement accounts and 20% of our income to paying off the house. We are contributing so much to our retirement accounts to keep us from falling off one of the Obamacare cliffs at 200% of FPL. If it weren’t for the Obamacare cliff I would reduce our retirement accounts and put more on paying off the house.

It’s extremely difficult to project what our income will be for the year and throughout the year, and with only 1 employer of my 3 offering a 401K, my math can end up being off by a bit. This year our AGI ended up almost 3K under that magical 200% of FPL number. Next year I will take action to get a bit closer, diverting even more money to our house payoff. Mrs. C. should have a 401K through her work this year, which will allow us to put up to 75% of her income into it if needed, providing additional flexibility.

Since our taxable account by definition does not help us on our taxes and it is essentially “extra” investing, I am OK with hitting the pause button until we pay off our house. This will give me $1,200 more per year to divert towards the goal of paying off our home by the end of 2020.

For the 2 years I have had the Betterment account it has given a time weighted return of 44.8%, compared to the S+P 500 at 46.9%.

Tesla: I am long on Tesla and I wanted to put my money where my mouth was. I think Tesla will be one of the highest market cap companies in the world by 2025, as it spearheads the transition to electric vehicles, solar power, and batter backups. I invested around $12,000 in Tesla between June of 2016 and January of 2017.

eBay: I had a small amount of cash in one of my brokerage accounts and used it to buy 2 shares of eBay, rather than sitting as cash forever. Obviously this won’t grow to any large portion of my portfolio.

House Payoff:

We took another step towards paying off our home early with a $3,000 end of year payment to our principal balance, on top of the $200 per month extra and a $7,500 principal payment back in June. Our current mortgage balance is $70,812. We also still owe $22,628 on our other house which Mrs C.’s mom lives in and pays the house payment on. We are on track to pay off our mortgage at the end of 2020, 36 months from now, and the mortgage on the other house 6 months later, making us completely debt free on my 35th birthday.

Our earliest finish is May of 2020, our most likely finish is December of 2020, and our late finish is May 2021. From our early finish to late finish projections the difference in total interest paid is only about $1,200, which is equal to the total interest we paid in the first 3 months of our loan. Paying off the mortgage about 2 decades early will certainly feel good!

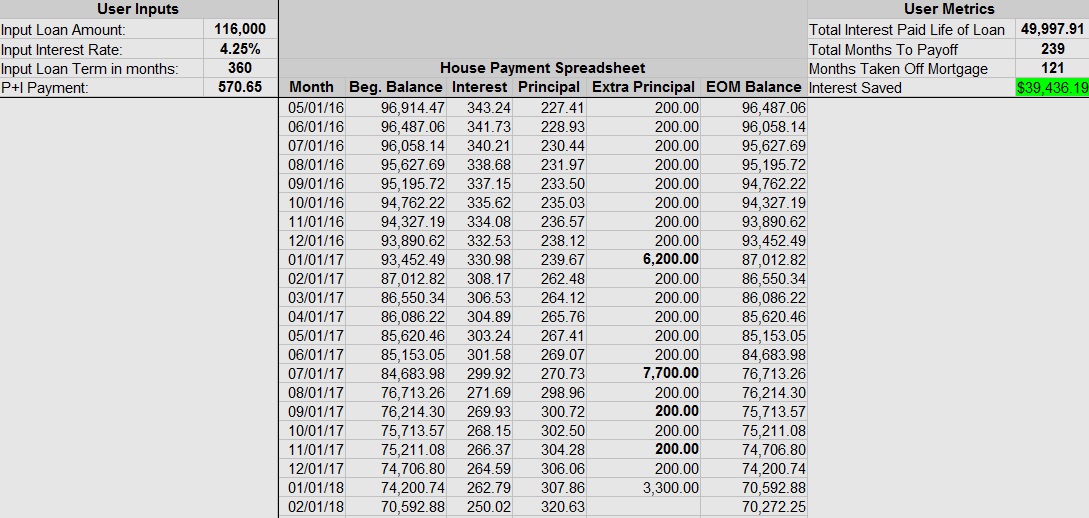

I track my mortgage payoff with a mortgage spreadsheet I created. With how long term the goal of paying off my house is, I made this spreadsheet to help keep me motivated. It shows me exactly how many months I have taken off my mortgage and how much interest I have saved to date. If I never make another extra payment I have already taken 10 years off my mortgage and saved $39,439 in interest. The slight discrepancy between the end of month number on this chart and the total balance remaining I reported above is due to the actual January 1st payment not coming out yet, but with the extra $300 monthly payment and $3,000 end of year payment coming out.

Skymiles and Points:

Skymiles balance: 165,494, this will be reduced greatly as we plan to use the vast majority of this for our hotel on our 2018 Disney trip. We don’t have a high demand for flights, as my employer directly pays for all my work flights and Mrs. C. has no desire to ever get on a plane. Add in that we would need 6 tickets to go anywhere as a family and our Skymiles are much better spent on lodging, even though the cents/mile is much better for flights.

Choice Points: We are in the process of racking up Choice points for future vacations. Our Choice Privileges Visa card has no annual fee and we use it for virtually all of our expenses. So far we have 57,371 points, almost enough for 6 nights at many hotels.

Hilton Honors: We have 122,000 Hilton Honors points. Most Hilton hotels are in the 20K to 35K range for redemptions. There are 2 hotels for 10K points that are strategically located for us. 1 in Bowling Green, OH which is perfect for trips to Toledo, Detroit, and Cedar Point, and 1 in Seymour IN which is a little past halfway to my parents house. Having 120,000 points then gives us about 10 free nights. I will continue adding to this balance as my employer often has us staying in Hilton hotels.

Action Economics:

This year Action Economics showed a modest increase in income. Our income was largely muted due to a change in how Amazon Associates operates which was implemented back in April. Instead of your earnings percent being based on number of items sold, it is now category based. I had been hitting a 7% tier, but now I am mostly getting 4% as the majority of the products I have links for are in 4% categories. This represents a pretty substantial cut. Net income grew from $2,033 to $2,489.

Earnings:

October Total: $133.19:

- Amazon: $133.19

- FlexOffers: $0

- Google: $0

November Total: $179.23:

- Amazon: $74.06

- FlexOffers $0

- Google: $105.17

December Total: $225.35:

- Amazon: $125.35

- FlexOffers: $100

- Google: $0

Traffic:

Traffic has done quite well this year and I am certainly happy with the growth. Total page views of 214,887 compared to 136,483 in 2016 representing a 57% growth rate. Organic page views of 132,870 compared to 85,436 in 2016 representing a 55% growth rate. Total articles on site have grown from 241 to 291. I would like to hit 250,000 page views in 2018. Total subscribers has increased from 131 to 374.

2018 Preview and goals:

1. Braces:

For 2018 we will finish paying for phase 1 of our oldest kids braces, with roughly $800 total remaining. Phase 2 most likely won’t start until 2019. He has one more adult tooth that needs to grow in first. We are planning on starting braces for Mrs. C, which will run about $7,000 total, 2018 should be around $3,000 with the remainder spread between 2019 and the first part of 2020. Another $1,000 will come out for a crown Mrs. C. needs. That’s almost $5,000 on dental expenses next year.

2. Pay down our mortgage:

Our goal is to hit $15,000 in extra principal payments on the house this year, leaving us with just over $50,000 in primary residence debt at the end of the year.

3. Add to our investment accounts:

We should also add in excess of $15,000 to our investment accounts, allowing us to cross into six figure territory. The first $100K is the hardest!

4. Visit Walt Disney World:

We are planning to take a trip to Walt Disney World in late August. The crowds are much lighter this time of summer compared to the rest of summer as kids across the country are returning to school. Since Michigan schools don’t start up until after labor day we have a good opportunity to avoid some of the crowds. We will be getting 6 day tickets, planning in a rest day and visiting Kennedy Space Center for a day during our trip. This trip is being entirely financed by Action Economics earnings. So far I have just north of $2,000 in our separate account for this trip. As mentioned above we will use our Skymiles for lodging during this trip.

5. Teach Kid #4 how to ride a bike without training wheels:

We are extremely close on this one. He can balance extremely well on a balance bike ( a training bike with no pedals), and he can bike with training wheels, we just need to put the two of those skills together and get him riding with no assistance.

6. Replace “The Death Hoopty”?:

My sister in law has dubbed my car “the death hoopty”, based on how sketchy it feels driving at times. She had borrowed my car for a week last summer and did not feel comfortable driving it. Mrs. C. says she would be shocked if my car makes it through the year. My car is a 2000 Toyota Corolla that we picked up 3.5 years ago for just over $1,000. It has 240K miles on it and has a few mechanical issues that aren’t really worth fixing on it. I don’t put a ton of miles on it. At a minimum I would like it to last through my fall outage season. Ideally it will hold up until we get our tax return in 2019, which should be north of $3,000 thanks to the recent tax overhaul. That would give this car a very respectable 5 year run and won’t cause us to drain down any savings to replace it with something much better.

My sister in law has dubbed my car “the death hoopty”, based on how sketchy it feels driving at times. She had borrowed my car for a week last summer and did not feel comfortable driving it. Mrs. C. says she would be shocked if my car makes it through the year. My car is a 2000 Toyota Corolla that we picked up 3.5 years ago for just over $1,000. It has 240K miles on it and has a few mechanical issues that aren’t really worth fixing on it. I don’t put a ton of miles on it. At a minimum I would like it to last through my fall outage season. Ideally it will hold up until we get our tax return in 2019, which should be north of $3,000 thanks to the recent tax overhaul. That would give this car a very respectable 5 year run and won’t cause us to drain down any savings to replace it with something much better.

How was 2017 for you? What goals do you have for 2018?

Leave a Reply