How To Hire Your Kids, We Hired Our 3 Minor Kids!

How to hire your kids

For the past 7 months we have been dabbling with an online Amazon FBA business. With school ending and my busy spring refueling outage season behind us now was the perfect time to hire our children who are 8, 9, and 12. Our oldest who just turned 18 is in the process of searching for a real job, which will come with more hours and more total compensation. For the most part children that are yours or that you are the legal guardian of can be hired in a family business regardless of age so long as it is 100% owned by the parent / legal guardian. There are some caveats here, such as the work has to be legit for the business and the pay must be comparable to the work done. You can’t hire your kids in your business to do household chores, nor can you hire a 3 year old and pay him $100 an hour to be a marketing manager; it has to make sense.

Why Would You Hire Your Kids?

There are several benefits to hiring your kids, including:

Skill Development: Hiring your kids gives them practical soft skill and hard skill development. These kids are learning to work together, show up on time, and have a good attitude. They are also learning how to scan items using an app, how to perform cashier transactions, and how to run an e-commerce store. When my kids enter the “real workforce” They will have almost a decade of work experience over their peers. Although my youngest is 8, I would consider hiring a kid as young as 5 in this business.

Tax Shifting: If Mrs. C. and I do 100% of the work and claim 100% of the income from this business, then our marginal tax rate would be over 40%. 22% federal income tax, 15.2% self employment tax, and 4.25% state income tax. Minor children employed in their parents business don’t have to pay payroll taxes, are exempt from federal income taxes if total income is below the standard deduction (currently $12,550), and all they have to pay is the 4.25% state income tax. Hiring our kids and having them do the work lowers the effective tax rate by over 35%!

Work Shifting: Hiring our kids allows us to focus on bigger picture items while the kids handle the grunt work. It also allows our time to be magnified. If Mrs. C. goes to scan books somewhere she might be able to scan 300 books in an hour. With 3 kids each scanning an average of 200 books an hour, the amount of Mrs. C.’s time spent in the book store is reduced by two thirds. She can now go to 2 other locations in the same amount of time. Our business can expand quicker.

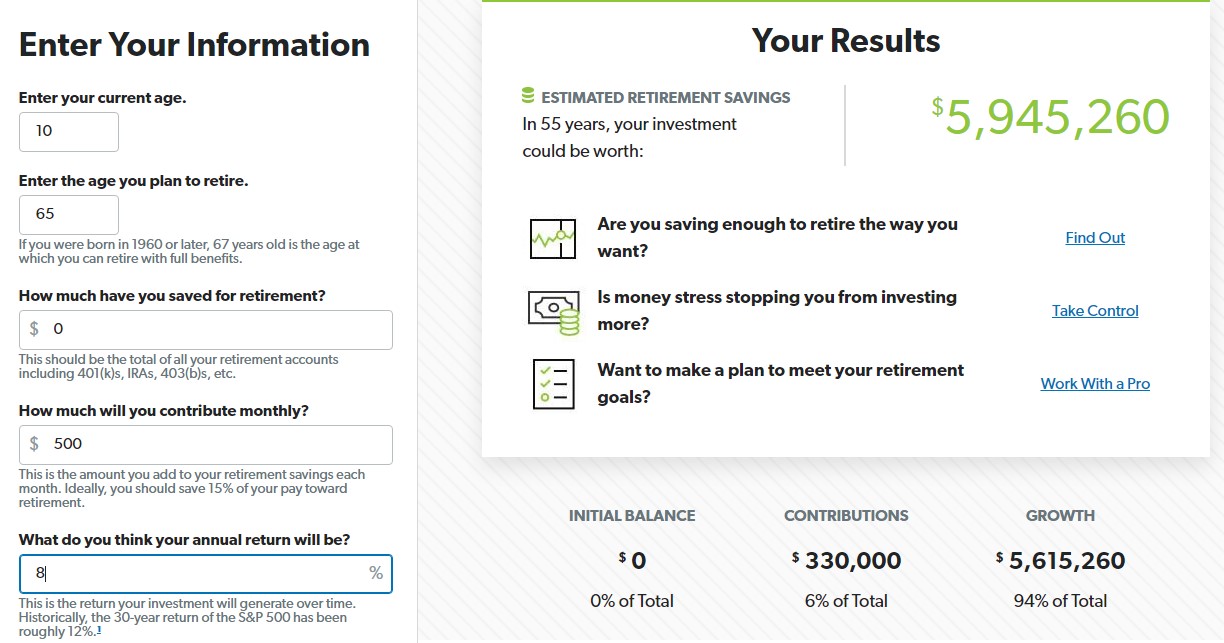

Roth IRA Investing: Starting investing earlier leads to exponentially higher rewards. Let’s assume a steady investment rate of $500 per month and a retirement age of 65, with 8% annualized returns. Someone starting at 40 would have $475,000, starting at 30 would have $1.1 million, starting at 20 would have $2.6 million, and starting at 10 would have $5.9 million. (10% returns would grow to $660,000, $1.9 million, $5.2 million, and $14.3 million respectively.) Having earned income is a requirement to start a Roth IRA, an investment vehicle with a current limit of $6,000 per year that will never be taxed. When you hire your kids in your business it allows them access to this investment vehicle.

Hire Your Kids Roth IRA (Calculator image from RamseySolutions.com)

This is the best way to build generation wealth. I’m not handing the money to the kids. They have to earn it through adding value in the market. I’m providing the system and the coverage. I set up the system wherein they can make the money and hired them. I provide coverage because I am covering all their expenses, so they have the ability to invest virtually all of their income. Starting at 10 instead of 30 will result in them accumulating several million dollars in wealth!

Efficient Generational Wealth Transfer: Mrs C. and I are on track to be able to fully fund my 401K and both of our Roth IRAs, leaving us with no other tax advantaged accounts to contribute our money to. Any income we could earn from this business therefore could not be saved and invested in a tax advantaged way. The children earning income opens up the potential for $18,000 of additional tax favored accounts for our family. If we earned this money, we would pay a 44% tax rate, then we would have to invest it in a taxable account, then upon our deaths our children would have to pay another 40% inheritance tax on the now much larger amount of money, at which time they would all most likely be senior citizens. This system of them earning money in the business we set up and contributing to Roth IRAs is much more efficient. Mrs. C. and I can also contribute matching funds to their Roth IRAs so long as their earned income is at least equal to all Roth IRA contributions.

Delayed Gratification and Investing Knowledge: Delayed gratification is one of the most difficult skills to learn, but it is so important to success in all areas of our life, not just financial. Having to wait until the end of the month for a paycheck teaches delayed gratification. I work with many adults who can’t stand a 2 week pay period. This is teaching delayed gratification. If my kids get a job that pays every other week they will think that is an amazing deal. Investing 75% of their money and tracking it over time teaches delayed gratification. Making investing decisions every month teaches investing knowledge. The more they work their investing muscles the more they will grow.

Credit Building: We have a credit card that we use for this business that we will add the kids to as they turn 13. Some credit cards allow kids of any age to be added to credit cards, but ours limits them to 13. This will give them 5 years of credit history by the time they are adults. Over the next several years this business could/should grow and at 16 and 17 their earnings could grow to be well over the $12,550 max for the standard deduction. Having 2 years of solid earnings as well as 5 years of credit history could allow them to buy a house at 18, without taking a withdrawal from their Roth IRA. This wouldn’t necessarily be a house for them to live it, it could be their first flip or rental property.

How To Hire Your Kids:

Start A Business: Give your business a bank account (it can be a sub account under your main account) with a debit card. Seed the business with a few hundred dollars of working capital. Start doing something. You don’t have to re-invent the wheel. Mow lawns, baby sit, pick up trash at commercial buildings, paint street numbers, power wash, retail arbitrage, or any of a thousand other ideas. Just do something that requires labor and is needed in the marketplace. Ensure this is something that young children are capable of adding value to so that you can hire them to do a majority of the actual work.

Get a Federal Employer Identification Number (EIN): This is simple enough and only takes about 15 minutes, it can be done online and they give you the number immediately. For sole proprietorships, which is what this is, you only get 1 EIN to cover all your business activities, so if you start other business ventures they will still be covered by the same EIN.

Register With Your State: In Michigan you must register your business with the Department of Treasury and with Unemployment. You also have to register each new hire. When registering at the Department of Treasury it will send you to register with the Michigan Department of Labor for unemployment tracking and taxation. The department of labor will then send a notice in 7 to 10 days. Unemployment taxes are due quarterly, in theory employing only your minor children will keep you exempt from these taxes. I need to do a bit more research on this, perhaps we are exempt from federal unemployment taxes but not state.

The department of treasury will ask you to estimate the total of employee state taxes that will be paid in, and then it will assign you how often to make payments. You can always make payments in advance.

When registering employees at MI-newhires.com the online form will give an error message if you enter a birthdate that indicates the employee is under 10 years old. Your child employees do not have to be 10! You can actually skip this question because it is optional! They have an option to download a spreadsheet and submit your new hires that way, which will also work to navigate around the error message. This is also easier to do if you are hiring multiple people.

The overall process of state registration was frustrating and I didn’t have all the answers I felt I needed. I felt a little overwhelmed and it took multiple hours. Yeah it was frustrating, but in the end it’s well worth it. I made it happen and you can too.

Required Paperwork For Hiring Your Kids:

- New Hire Letter: When I hired my kids I gave them all a new hire letter. This includes a detailed job description, rate of pay, and start date, with a spot for them to sign. We are starting all the kids at $10 per hour. As they become more valuable we may increase their rates.

- I9: All employees must fill out an I9 that you keep on file. Minor children have more document options than adults. I filed their I9s out with their Social Security cards and a medical record as verifying documents.

- W4 and state W4: W4 forms are for tax withholdings. For the federal W-4 form your children can write EXEMPT under line 4(c) because they had no federal tax liability last year and expect no federal tax liability this year.

- Hour tracking log: I made a simple spreadsheet for tracking their hours. I have a different one for each month. At the end of the month I will tally up their hours before issuing their checks.

- Paystubs: I designed my own paystub as well. Take a look at one of your pay stubs and copy it. These will get printed out every month. My kids will be paid once a month to simplify accounting.

- Record Keeping: When you hire your kids you need to keep your records. You need a place to keep all of these documents together, I use a large binder. I would suggest keeping hour logs and paystubs forever in case the IRS ever wants to audit you. You also need to track all the income and expenses of the business venture. Make sure to keep your personal finances separate. It’s also a good idea to print yearly bank statements and Roth IRA statements showing where the money is going. The IRS looks for people who “hire their kids” but in reality the kids do no work and the money goes towards household expenses. The parents are effectively committing tax fraud to use up their child’s tax brackets.

Payroll Planning For Hiring Your Kids:

We are paying the kids once a month using the paystubs we designed and the hour tracking log. We will then transfer their net pay from our business bank account to their bank accounts. Directly after they receive this pay, we will then transfer 75% of their paychecks to their Roth IRAs. We will then withdraw the rest for them to be able to spend 25% of their pay. We decided on this 75/25 split because if the kids never see the money they won’t be motivated to keep working. Even showing them the growing balances in their accounts will not be enough. They need some immediate rewards. The split also gives us the option to at the end of the year give them a bonus deposit to their Roth IRAs from our bank accounts if they have earned $6,000 but not reached $6,000 in their retirement accounts. If they have $4,500 in their accounts and earned $6,000 we can deposit $1,500 of our money into their accounts and be legal.

We will keep track of their Michigan state withholdings and send in payments quarterly. If their earnings were above the $12,550 limit then we would need to start withholding for federal income taxes.

After You Hire Your Kids Set Up A Roth IRA!:

After you hire your kids you want to set up a Roth IRA for them. Fidelity makes it easy to setup a Roth IRA for minor children. I set up accounts for all 3 kids on the same day and it took less than a half hour. When I setup the first account it let me set up a username and password. I thought that this would be unique for each child, but it is not. The username and password is for the custodial account for the custodian. Because I am the custodian of all 3 accounts, they are all sub accounts inside of my account. So when I log in, with my username and password I can see all 3 accounts.

If you have multiple children ensure that you give nicknames to each account. The accounts will simply list the account number and say “Roth IRA MINOR CHILD” Adding the kids names to these will make it easy to track actions for them so you don’t get them mixed up. Also ensure when nicknaming the accounts that the correct account number gets the correct child as the nickname.

Equipment For Child Employees:

The older 2 employees already have cell phones, so we didn’t need to purchase these. We bought each child a Bluetooth Barcode Scanner, 2 car chargers, and portable battery charger to allow them to do this work effectively. We also paid the $34 a month for the Accelerlist program to be able to greatly streamline the process for listing Amazon FBA products to send it to Amazon. The total cost of all new equipment we had to purchase for the business was under $200. The paperwork and cost to hire our children was nothing except a day of my time.

Cautions For Hiring Your Kids:

Their income may still count as household income for means tested programs. This income could potentially cause reductions in needed assistance. Keep this in mind and do the math / check with your case worker before implementing. This includes programs such as Medicaid and CHIPS (MiChild in Michigan). If you hire your kids and it negatively effects your total household income, then we are moving in the wrong direction. We also need to balance long term wealth building with immediate needs.

Their income could cause them to have to file a tax return: This is extremely important. If a child is required to file a tax return then their income counts towards total household income and is reportable for ACA health care plans. This can not only cause substantial increases in premium costs, it theoretically could push your household over an Obamacare cliff, causing premiums to skyrocket and perhaps the loss of any subsidy. If your family is covered by an ACA plan, then you do not want your children to be required to file a tax return. This means total earned income must be under the standard deduction ($12,550) and total self employed income must be under $400. This can also get complicated if the children receive Social Security survivor benefits (two of my kids do).

Hiring Your Kids Could Negatively Effect FAFSA Qualifications: When filing out the FAFSA for college financial aid parental resources and child resources are evaluated differently. The expected family contribution based on parental assets is 5.65% of non retirement / non exempt assets, and between 22% to 47% of eligible income, which is income over a fairly generous base.

Student income is assessed at 50% and assets are assessed at 20%. BUT qualified retirement accounts such as Roth IRAs are exempt from the calculation, so they should be fine on assets. This is important because if you were investing money for the kids in a taxable brokerage account (UGMA) such as stockpile, those assets would be considered available for FAFSA and they would need to spend 20% of those assets on college costs. Yeah I know the FAFSA has a lot of complicated math, but the big picture is that student income and assets are assessed a higher contribution percentage than parents income and assets. Check out the book Paying for College, 2021: Everything You Need to Maximize Financial Aid and Afford College for in depth FAFSA information.

If you follow my guidelines are are paying them right around $6,000 a year to max their IRA then the expected family contribution from their income would be $0 because the current protected income level for a dependent student is $6,940. They would have no expected contribution from their assets because their assets should virtually all be in their retirement accounts. Receiving financial aid is also not super important. Financial aid maxes at $6,495 per year in 2021. This is certainly a significant amount of money, but compared to stashing $6,000 per year into a Roth IRA every year from 10 to 18, is relatively minor. For my kids who are covered by the Benton Harbor Promise Zone, Pell Grant eligibility isn’t necessary for the first 2 years, since the promise zone will cover their first 2 years at a community college, so really we are only at risk of losing 2 years of Pell Grants rather than 4. Most likely by the time we fill out FAFSA forms our income and assets will already prevent our kids from receiving Pell grants.

Conclusion:

Hiring your kids is a great idea to teach life skills and to build massive generational wealth. To hire your kids you don’t need an existing business or to run a business as your full time occupation, a small side hustle can serve as the business for hiring your kids. The hassle factor involved is well worth it to establish Roth IRAs for your children and get them building a work ethic today.

What do you think about hiring your kids are you going to take the leap?

Leave a Reply