How We Set Up An Apartment For Kid #2

Kid #2 is turning 18 and is in a unique situation. He graduated high school early in November of 2024 and has been working full time since March of 2025. He started working part time when he was 14. He is in a much better financial position than most people 10 years older than him, and at this point moving out makes sense for him. In general I am not in favor of young adults moving out at 18, but because he has been working for 4 years and graduated from high school almost 2 years ago, based on milestones it makes sense. Since we are moving him into one of our properties it makes even more sense because it isn’t fully being on his own and allows us to reduce his cost of being semi-independent.

Current Rents In Our Area:

There are very few houses that have come on the market in our area recently. A 2 bedroom house is generally running around $1,200. For apartments I go off of Briarwood Apartments, which is a large apartment complex in Benton Township that publishes their rates. As I am writing this the current rates for a 1 bedroom apartment that is 550 square feet they start at $856/mo. For a 2 bedroom apartments that is 680 square feet they start at $1,027.

Kid #2 has been a strong saver, but his income is on the low end and a rent payment this high would be very difficult. Although he would qualify for an apartment, a typical apartment would leave him with very little ability to keep saving and investing. He also is less likely to be chosen as a tenant even if he qualifies due to relatively low income and low credit history.

Our First Home:

In 2006 Mrs. C. and I bought our first home for $48,500. This was a fixer upper 5 bedroom 2.5 bath 2000 square foot home in St. Joseph Township on the border of Benton Harbor. We lived in this house for about 6 years, rented it out for a couple years when we had trouble selling it, then Mrs. C.’s mom lived there for about 5 years. We turned it into a rental again at the end of 2019 and recently had a long term tenant move out.

This house was once a Duplex and we started exploring the idea of turning it back into a Duplex in order to have an affordable apartment for our kid to live in, while still generating income from the property.

Finances:

We effectively paid this house off years ago, however we rolled the financing of our next 2 rental houses into a 15 year mortgage on this house in 2019. We currently owe a bit under $48,000 on the 4.75% 15 year mortgage with a payment of $552 per month. Our property taxes are roughly $135/mo and insurance is $100/mo, for total payments of $787 per month.

As a single family home we have had the property rented out at $1,400 per month. This is fairly low for a house of this size. This house was built in the early 1900s and although it is clean, safe, and functional, it is rough around the edges.

Originally we did not qualify for a loan. We were denied a loan application at the last minute in 2006. Do you know how bad of a credit risk you had to be to be denied a mortgage loan in 2006? We were putting down 20%, but I had no credit and Mrs. C. had some bad credit items. We were also both classified as “part time” employees, even though we were working 39.9 hours per week. The mortgage broker we were working with underwrote a loan directly through his company after the big bank denied us. Our first loan was for $38,800 at 10% interest with a 1 year balloon, and we needed to fix our credit in that year. to refinance out of that loan with a big bank.

A year later we refinanced and took some cash out to cover the roughly $6,000 of closing costs and to pay for adding carpet in a few rooms. This loan was a 7.37% on a 15 year mortgage for around $47,000.

We waited WAY to long when rates dropped to refinance. We thought we were going to sell the house and it didn’t happen. We got our 3rd loan by refinancing to a 10 year at 3.5%. This would have been around 2013. We did not take any cash out and the main reason for the refinance was to make the monthly mortgage lower while Mrs. C’s mom lived there.

Then we got our FOURTH loan on the house in 2019. The mortgage was close to being paid off and we did a cash out refinance to cover the purchase and rehab of our next 2 rental properties instead of getting small individual loans for them. This is the current loan we have for $552/mo. This loan is scheduled to pay itself off in 2034. Currently about 2/3 of the payment goes to principal repayment.

Splitting The House Into A Duplex:

Unfortunately there is no good way to separate the utilities, so we will have to estimate the utility costs and include utilities in the the rent. To get started we are using the following estimates:

- Water/Sewer/Trash: $70

- Natural Gas (Heat and Water heater): $130

- Electricity: $200 ($100 per apartment)

If the real numbers are lower or higher we will adjust this portion of the rent in a year.

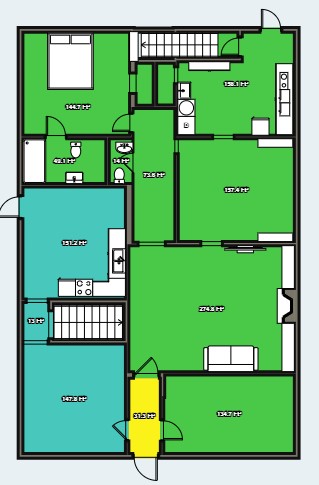

We cut the house into a 3 bedroom apartment and a 1 bedroom apartment.

The 3 bedroom apartment has a large kitchen and dining room downstairs with an exterior entrance from each room. This unit includes the entire upstairs that has 3 bedrooms, a full bathroom, and a small office room.

The 1 bedroom apartment has a bedroom with a full bath attached to it and a tiny 1/4 bath (sink and toilet). There is a kitchen, a dining room, and a large living room. We could have made the living room a 2nd bedroom, but it would be weird with the only shower being in the other bedroom. In the future we may change the layout for this to be a 2 bedroom by walling off the master bedroom’s access and losing the 1/4 bath.

We tried several iterations of how to split this house up and this was the best one we could come up with. This maximized the value for both units, while minimizing disturbance between the two. The 2 kids bedrooms upstairs are over the living room and kitchen for that unit, and the parents bedroom is at the opposite end of the house as the bedroom for the 1 bedroom unit.

The 3 bedroom apartment is roughly 950 square feet. The main downside is that both the kids bedrooms are fairly small.

The 1 bedroom apartment is roughly 900 square feet.

The Green Rooms are Kid #2s unit, including the front porch in the lower right hand side. Originally the Blue kitchen opened up to the hallway and the blue living room (lower left) opened up to the green living room and was used as a dining room.

The entire upstairs is for Unit 2. The room at the end of the hall (top) has slanted ceilings so it does not qualify as a bedroom due to being about 20 sq shy. We used it as a bedroom several times when we owned the house. We now have it labelled as an office.

The 1 bedroom has a lot of extra square footage in this situation, but I wanted to preserve 2 doors for direct egress for both units, and this was the only way to do so without really cutting up the house. If I went that route I would be more inclined to add a bathroom and make this a triplex.

I plan to rent the 3 bedroom unit at market rate. So what is market rate? Well we established that a 2 bedroom with 250 less square footage and no utilities included is over $1,000 a month. If I just go with the apartment being worth $1,000 and adding in the utilities we estimated, the total rent would be $1,200/mo. The net income to us after utilities is $1,000, just $200 less than what we were just renting the house out for.

To make this split work we need to:

- wall over a doorway from the kitchen to the hallway

- wall over a doorway from the dining room to the living room

- Build a wall on the front porch to separate the main section of the porch

- Install a privacy fence separating the backyard sections for each unit

With all of these moves we did not permanently alter the structure, so if we want to return it to a single family house we can do so relatively easily.

I chose to leave the trim framing around the doors to make it easier to switch back if we ever decide to. The 6 unit apartment building we have is the same way with a few of these walled off door locations.

The Cost:

The cost to do this was actually relatively low. I had several 2 X 4s and 2 X 6s available from another project, so the wood for the framing was free. I blocked off two doorways and created a partition on the front porch.

I spent roughly $120 on a door, $100 on drywall, and $60 on paint.

We did need to change the layout of the deck leading to unit 2, but that deck was well over 20 years old and needed replaced anyways so I am not including that cost in here. I have not installed the fencing yet, but it will require 8 4X4s and 7 panels for a rough cost of $700.

Most of the cost and time of this project was other work we needed to do to the house due to damage from the previous tenant as well as general aging. I had to replace a lot of the subpar work I did almost 20 years ago as a young man. In total we spent over $7,000 across 3 months on this property. This did include almost $2,000 on a combo washer/dryer in order to have laundry without needing to add a 240V outlet.

Subsidizing The 1 bedroom:

The 1 bedroom should be worth about $300/mo less than the 3 bedroom, which would put it at $900 with all utilities included. This would make the actual rent portion $700/mo. We are planning to charge our kid $400 total, for a $500 per month subsidy.

Compared to the $1,400 we were previously renting the house out for with both units rented out and excluding the $400 for utilities, the total rent would be $1,700/mo. Since we are paying for utilities our actual earnings from the property should be around $1,300, only $100 less per month than we got with our last tenant.

By turning the property into a duplex we have increased the total of what we can earn from the property in the future. We can maximize for this later on. Just the income from the 3 bedroom covers the expenses for the house.

It is very common for parents to pay for their kids housing in college: Many parents pay for dorm rooms for 4 to 5 years. A single room at MSU runs about $9,000 a year. Subsidizing an apartment we already own is far less expensive than most dorm rooms. This subsidy would of course come with strings. The difference would have to continue to be saved and invested for the long term. Over the years we have subsidized the rent of Mrs. C.’s mom and two of her sisters, if we would do that for them for several years, why shouldn’t we do the same for our kid? There is a lot of value to being able to influence the savings rate of our young adult children.

What We Gain:

The primary #1 thing we gain is that Kid #2 is able to save more money into his Roth accounts than if he was paying market rent elsewhere. I really want all our kids to have $85,000 before they move out, and he is quite a bit shy of this, but he is also moving out about 4 years sooner than expected. He is doing great and WAY advanced for his age. He needs independence and some more space. With us keeping his rent at a lower rate than what he could get elsewhere he can continue to invest at a rate far exceeding normal. While living at home he was investing 50% of his net income in his Roth IRA (and was saving another 25% in cash), now he is on pace to be saving 40% into his Roth accounts. This is the most important benefit of this. He is still able to move out and continue to save at a high rate.

We gain a 150 square foot bedroom in our house. Our house is roughly 1800 square feet. We originally bought it as a family of four, however the vast majority of the time it was been higher than that. We peaked at a total of 10 for about 6 months, and our normal has been 6. When he moves out we will be back down to 4 and regain this large room. Regaining this room will give a lot more utility to our library room and craft room, which are both bursting at the seams. What would you pay to increase the usable square footage of your house by 150 square feet? A climate controlled storage unit of this size is about $200 and not attached to your house.

We also gain the future revenue of this building being a duplex. We were not looking at turning this property into a duplex prior to looking for a solution for him to move out. Long term we will end up making way more income off of this property than we would have keeping it as a single family house.

If he stays in this apartment for 4 years, we will have moved 4 more years down the amortization of the loan and only owe $26,000 on the property. He will have saved the equivalent of 1.6 years of income (at a 40% rate) into Roth accounts and will be in a great position to buy a house or do anything he wants really.

What do you think about us creating this apartment for our son? Is this something you would do?

Leave a Reply