Paying For A Funeral

When a loved one passes the last thing you want to think about is money, but all to often an unexpected death leads to thousands of dollars in bills that the deceased didn’t have in their estate. This leaves loved ones footing the bill who also may not have the resources to cover the expense. When Mrs. C.’s sister died in 2014 she didn’t have any money and her parents weren’t in a financial position to pay any of the costs. This type of situation happens every day in America. Here’s how to save money on funeral expenses, and how a little bit of planning can go a long way.

Government Assistance:

I think that this is a major gap in our Social Security system. Social Security will provide a 1 time death benefit of $255. This is well under 5% of the cost of a normal funeral. Social Security introduced this death benefit cap in 1954, and the average payment at the time was $208. In today’s dollars this average payment is the equivalent of $1,886.

Although it would cost the system more money than it pays out now, it is still a major “deal” on the side of the government. When someone has paid into Social Security all their working life and is now deceased, they will not be collecting retirement benefits at all. Seeing as how the average retirement benefit is $1,180, a $5,000 death benefit would be covered with less than half a year of payments. I think at least providing this coverage to people who have not reached retirement age is necessary. It’s a relatively small portion of our population and they NEVER RECEIVE RETIREMENT BENEFITS. With the average person living into their mid 80s, that’s over 20 years of Social Security payments, or $276,000 of Social Security benefits. Clearly a $5,000 death benefit is much cheaper.

This type of policy change no matter how much it makes sense is unlikely to occur, so it is paramount to take action to prepare for your death or the death of those you care about.

Pre-Planning:

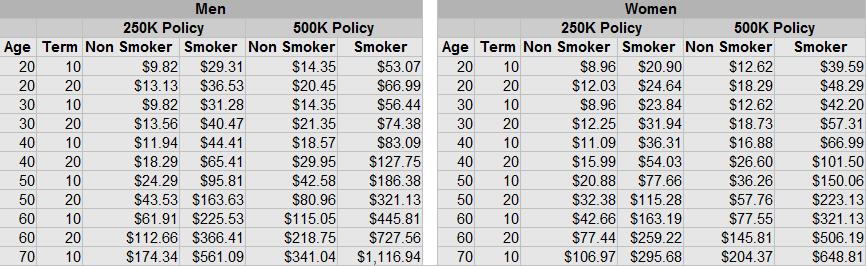

Step 1: Life Insurance: You need life insurance period. Get life insurance for yourself. Look at the people you care about. Is there someone you know who really should have life insurance but feels they can’t afford the premiums? Consider gifting a policy to them (with someone other than yourself as the beneficiary so they won’t feel like you have ulterior motives.) Life insurance is the number one method of paying for a funeral, and a good term policy will generally provide a lot more than burial expenses, which can take the pressure off of finances when people are grieving a loss.

Term life insurance for most people is insanely cheap. I picked up a $500,000 20 year term policy for $20 a month. The “sweet spot” in the term insurance market is $250,000 policies with 10 year terms. Most policies with lower payout amounts don’t have a scaled decrease in premium costs, for example a $100,000 10 year policy might cost $8 per month, while a $250,000 10 year policy might only cost $10 per month. These policies are so cheap because the likelihood of most people under 60 of dying in the next 10 years is fairly low, but it does happen. I can list dozens of people I know who died young, as I’m sure you can as well. You can get a quick easy quote without providing any identity information from Haven Life in just a few minutes. I made this chart below in 2014 and since then rates as a whole have actually lowered, so you could potentially get an even lower price.

For older people or others in poor health you can still get life insurance, just not in large amounts, this type of life insurance is typically called burial insurance and it is much more expensive as a percent of the payout cost, however the premiums are much more affordable than a large term policy and most people can get coverage. Keep the coverage down to the minimum needed to keep your loved ones from having to face hardship. The ultimate goal should be to establish enough wealth that the policy isn’t needed. For example, buy a burial policy today, and over the next 24 months build up a nest egg of $5,000 to $10,000, then cancel the policy.

Ask For Help:

When Mrs. C.’s sister died she was handling everything with the funeral arrangements. After receiving an estimate for total costs from the funeral director Mrs. C. looked into state aid to help. The state of Michigan will provide up to $850 in assistance, but only if the total of the service is less than $4,400. Our total was a little north of $5,000. She talked to the funeral director and they were willing to lower their cost so that we could qualify for the state help. This 1 conversation saved over $600 on the funeral bill and $850 from the state of Michigan for a total savings of $1,450.

Crowd Funding: Many people set up crowd funding campaigns with varying degrees of success. Mrs. C.’s aunt set up a crowdfunding page for her sister, which raised close to $2,000. 3 of the donations made up 75% of the total raised, which were from other close family members. If money is an issue certainly reach out to other family members for help.

Options:

You ALWAYS have options. You do not have to buy a casket or an urn from your funeral home. You can purchase these anywhere and the funeral home must accept them. Funeral homes typically sell more expensive models. Costco has Caskets for under $1,000 and you can buy Urns most anywhere online for under $100.

Do you have life insurance or are you self insured? Have you ever had to step up and pay for funeral expenses for someone who died without an estate?

Leave a Reply