Setting Up My Betterment Account

I finally signed up for a Betterment account earlier this month. I’ve wanted to start one for a while, but I wanted to wait until I had enough cash flow and a solid enough bank buffer to be able to commit $100 per month, which gives me a lower fee than if I contributed less. For accounts under $10,000 the monthly fee is $3, unless you automatically invest at least $100 per month, then the fee is .35%, which is much lower when starting out. My plan is to slowly increase the amount I am putting in each month, then once the house is paid off, put all of the money I had going towards the house into this account. Mrs. C. and I will then use this taxable brokerage account as the main account to draw from during early retirement.

A Betterment Taxable Account Vs. IRA

I already have my traditional and Roth IRAs set up at Vanguard and am happy with the asset allocation and service I have there. I also have an HSA with Health Savings Administrators. With how much uncertainty exists over future tax laws I strongly believe that having a diversification of accounts is necessary, which is a strong reason why I chose to open a taxable brokerage account with Betterment. Our contributions to traditional accounts and our HSA has dropped us into the 10% federal tax bracket, which lowers the incentive to try to put more money into tax deferred accounts, especially when we are so close to maxing out our IRA and HSA accounts. With current tax laws long term capital gains are not taxed if your marginal rate is 10% or 15%. If this stay in place anytime we need to take money out in the future we will not owe any taxes on our gains.

Taxable Betterment Account As An Expanded Emergency Fund:

With a taxable account I won’t be penalized to withdrawal any of my funds. I may be taxed if I take out funds that have been held for under a year, but even then I would only have to pay tax on the gain, not the total. Taxable accounts are FAR more liquid than retirement accounts, even if my goal is to use the accounts in retirement. It’s good to know that I can use this account to purchase a vehicle, or pay for my kids college without having to jump through hoops or face large penalties and taxes.

One of the great tools that Betterment has is TaxMin lot selling, in which their algorithm ensures that when assets are sold, the least amount of tax possible is owed on it. Most brokers will use the FIFO standard of First In First Out when selling securities. With TaxMin lot selling Betterment looks at every transaction that has occurred and chooses the best shares to sell based on the price and date they were acquired. Obviously they first liquidate assets that qualify as long term capital gains, but since I am buying shares every month, and in the future, probably every week, there will be hundreds of different lots for their algorithm to choose from to find the shares to sell that will result in the lowest amount of tax possible.

Tax Loss Harvesting:

I would love to take advantage of Betterment’s Tax Loss Harvesting, but because I have IRAs and an HSA elsewhere I would most likely end up in violation of wash sale rules. If at some point in the future I choose to move all my investments to Betterment (with the exception of REITs, since Betterment doesn’t invest in them at all) I will be able to take advantage of tax loss harvesting and can cut up to $3,000 per year off of my gross income. I think I would actually benefit more from tax gain harvesting in the long run, it would be interesting to see Betterment tackle tax gain harvesting.

The Setup Process:

Setting up an account with Betterment is a quick process, from start to finish it was about 5 minutes. After clicking to sign up it is a simple 5 step process, and the first 3 get it started:

1. Enter your name and address: Super easy, hell google had most of this memorized and filled in the blanks for me.

2. Enter your identity information: All they need is your social security number, and your date of birth.

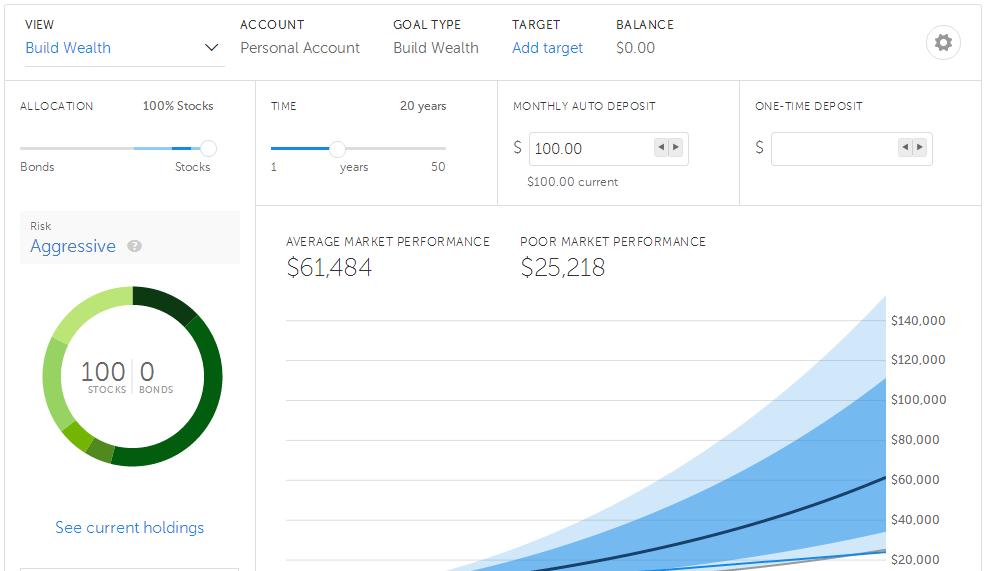

3. Set a goal: Set the stock/bond allocation you want. Then you can play with the interactive display that will show how your money will grow over time, depending on how much you put in per month. It is running some sort of monte carlo program in the background and tells you the percent likelihood you will have at least X amount of dollars.

4. Attach a bank account or rollover an IRA: Once again pretty straight forward. All I had to do was enter my routing number and account number. It takes a couple days for them to deposit two small amounts in your account in order to confirm the account, which is typical.

5. Assign Beneficiaries: Click on settings from the drop down bar on the upper left hand side, then click on accounts. I assigned 1 person (obviously Mrs. C) as a beneficiary, and 1 person as a contingency beneficiary. It’s extremely important to name beneficiaries for all accounts.

What Exactly Am I Investing In With Betterment Anyways?

The Vanguard investment split for a 100% stock allocation is:

- 41% International Developed Markets (Vanguard ETF: VEA) .09% expense ratio

- 17.7% U.S. Total Stock Market (Vanguard ETF: VTI) .05% expense ratio

- 17.7% US Large Cap Value (Vanguard ETF: VTV) .09% expense ratio

- 13% Emerging Markets (Vanguard ETF: VWO) .15% expense ratio

- 5.7% US Mid Cap (Vanguard ETF: VOE) .09% expense ratio

- 5% US Small Cap (Vanguard ETF: VBR) .09% expense ratio

This is low on small cap and mid cap domestic stocks and does not include REITs at all. My investments in our IRA accounts and our HSA balance this out because they are heavily invested in small cap, mid cap, and REIT investments. Betterment has a sliding scale from 0% to 100% stock allocation based on risk tolerance. Since I am primarily investing for the long term and don’t plan on touching any of this money for at least 15 years I have selected a 100% stock allocation.

Do you have an account with Betterment? How has your experience been with them?

Leave a Reply