Paying Extra On The House

Moments ago I made the first large step towards accelerating our mortgage. I transferred $5,000 to our loan, dropping our balance to below $100,000 and taking over 2 years off the back end of the mortgage. I originally wanted to throw closer to $10,000 at the house, but fell short of that goal. Hey, even getting halfway there is still a cause for celebration! For 2016 and beyond I want to be hitting 5 digits on these yearly deposits in order to have the house paid off by my 35th birthday.

Moments ago I made the first large step towards accelerating our mortgage. I transferred $5,000 to our loan, dropping our balance to below $100,000 and taking over 2 years off the back end of the mortgage. I originally wanted to throw closer to $10,000 at the house, but fell short of that goal. Hey, even getting halfway there is still a cause for celebration! For 2016 and beyond I want to be hitting 5 digits on these yearly deposits in order to have the house paid off by my 35th birthday.

Why Am I Paying Extra On The House?

Mathematically I could get a better ROI by investing the money in index funds. My mortgage is at 4.25% and the historic average rate of return for stock index funds is around 8%. I also already have a major chunk of my net worth in home equity and my house payment is an extremely small portion of our income at approx. 10%. With all of these factors against paying extra on the house, why am I doing it?

1. Reducing debt reduces risk: We don’t know what the future will hold. My mortgage amortization lasts until the end of 2041. The further out in time you project the less accurate the projections will be. Most likely I will be extremely financially secure and the mortgage payment would be a rounding error in our bank accounts if I kept it around….BUT I have seen many people who are in their 50’s who struggle to make their mortgage payments and have told me “If only I had paid off my house when I was younger.” That has some power to it. Income doesn’t always stay the same or increase. It is entirely possible that at any point numerous factors could cause our income to drop substantially. While I am having good years it makes sense to reduce my risk for future years.

2. A paid off house improves cash flow: Currently about 10% of my income goes towards the house payment. This year I put another 12% of my income towards paying it off early, and next year will be even more. Once the house is paid off it is done and all of that income comes back to spend on other things. One of the major question mark expenses in the future is paying for college for four kids. Having the house paid off and freeing up this cash flow before the first kid starts college will be a big help.

3. I’m already investing heavily in stocks: We are already contributing over 25% of our income towards our HSA and IRA accounts and will be on track to max those accounts in 2016. If we were not heavily investing in the stock market I would not be allocating as much cash towards paying off the house.

4. It feels right: Sometimes you just want something and the math takes a backseat. I like the idea of not having a mortgage. I want to know that the bulk of the largest expense in my life is done. I want the feeling that I truly own the ground beneath my feet and that even if I fall on lean months I don’t have to worry that I could lose the house.

How I Track Paying Extra On The House:

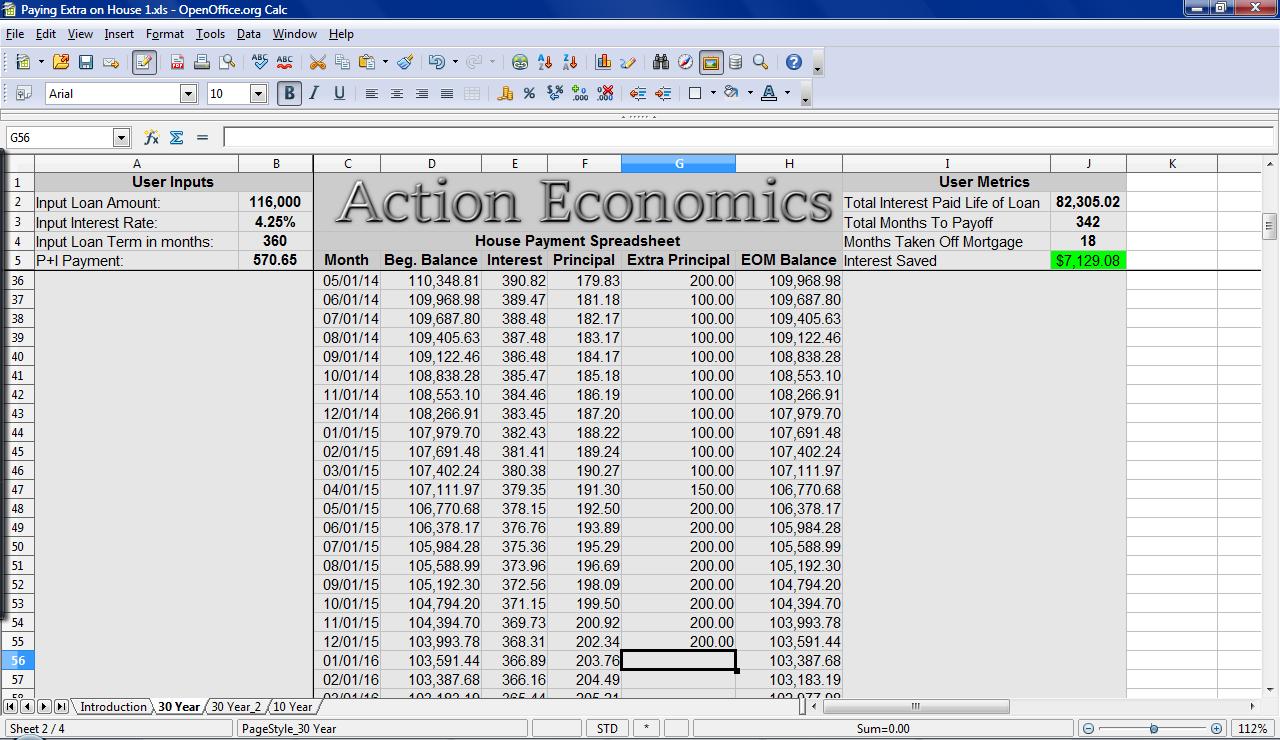

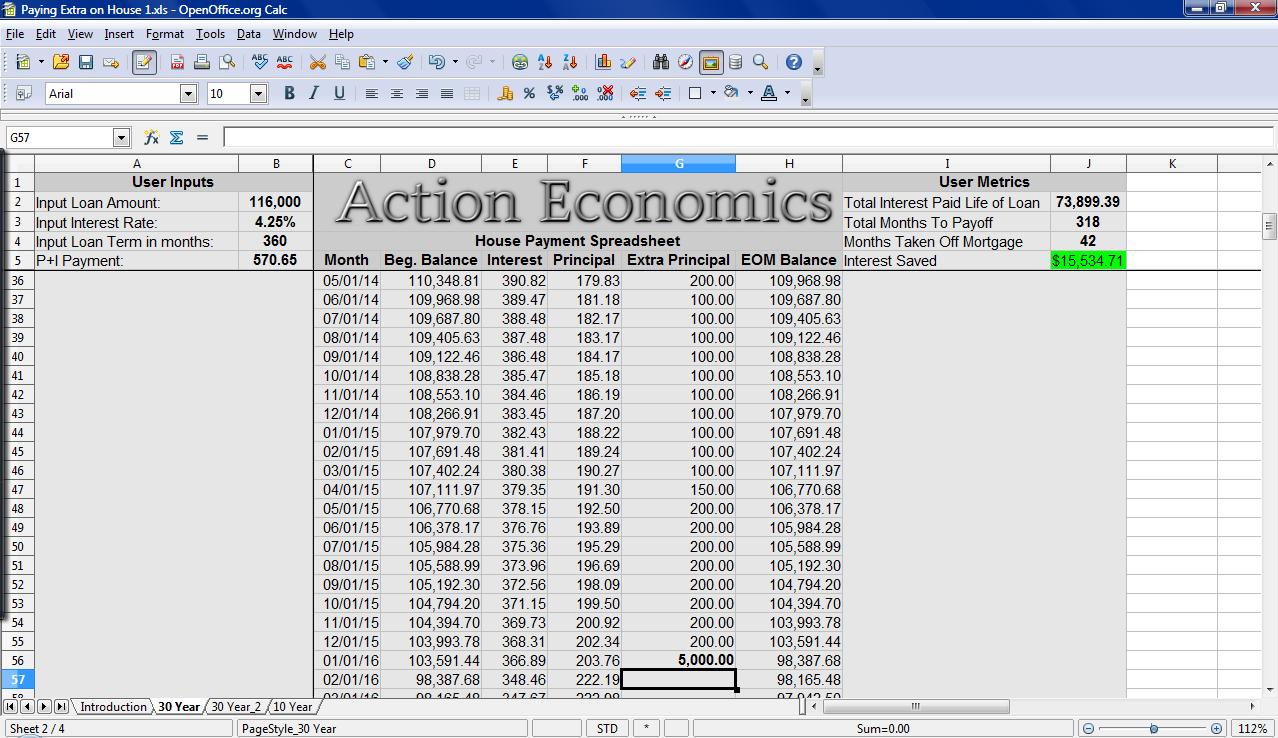

This year I spent a good deal of time revamping my house payment spreadsheet. The final product is the Action Economics House Payment Spreadsheet Version 3.0. In previous versions the main utility was to calculate an amortization table and input extra payments. Overall it was fairly useful, but the new version has a much greater utility. As you change figures in the extra payments column a user outputs section that is locked to the top of the spreadsheet calculates how much money in interest has been saved and how much time you take off your mortgage with each entry.

For example before making this $5,000 payment the total of all the extra payments I have made so far had reduced my mortgage by 18 months and saved me $7,135 in interest. Once I made this $5,000 payment the mortgage dropped to having 42 months removed from the amortization and my interest saved more than doubled to $15,534. Seeing this information update provides a huge motivational boost towards continuing to pay off the house, which is needed because without tracking it in this manner there is no reward until the entire mortgage is taken off, which will take several years.

Currently I am paying an extra $200 per month automatically and will continue to make a large deposit at the end of every year.

When Will Paying Extra On The House Pay Off?

In all reality it is paying off now by giving me the peace of mind of knowing I won’t have to pay a mortgage in later years. As you saw above, my total months saved thus far is at 42. This means my efforts so far have moved my paid off date up 3 and a half years. As time goes on the months saved will increase.

Another way that paying extra on the house is paying me off right now is in the increase in equity. Whenever extra principal payments are made the amortization speeds up and the mixture of principal and interest tips in my favor. last month I paid $368 in interest and $202 in principal. Next month I will be paying 348 in interest and $222 in principal. This is a $20 per month increase in net worth without having to increase my payments any more. Once again as time goes on this will continue to tip in my favor.

Of course the BIG payoff is when the mortgage itself is gone. I am currently aiming to achieve this by the end of May 2021 when I turn 35. Once again, even if I miss the goal by a year or two, so what? It isn’t all or nothing. If it takes me to May of 2023 to pay off my house I still did it 18 years ahead of schedule and saved a ton of interest!

What are your thoughts about paying extra on the house? Is it worth it, even though the return you are locking in is most likely significantly lower than stock market returns?

Leave a Reply