Building Generational Wealth The Complete Guide

I want my children, my grandchildren and my great grandchildren to be financially successful. I want them to be wealthy. I also want them to be smart, hard working, and kind. I want them to have enough resources that their predominate goal in life isn’t the accumulation of assets. I don’t want them to be stuck in a paycheck to paycheck lifestyle, or even a “spend my 20s and 30s killing myself to save $1 million” cycle either. I want to develop a plan of building generational wealth that will last for more than 3 generations and won’t cause the kids and grandkids to turn into spoiled trust fund brats. Here’s what I have come up with so far:

I want my children, my grandchildren and my great grandchildren to be financially successful. I want them to be wealthy. I also want them to be smart, hard working, and kind. I want them to have enough resources that their predominate goal in life isn’t the accumulation of assets. I don’t want them to be stuck in a paycheck to paycheck lifestyle, or even a “spend my 20s and 30s killing myself to save $1 million” cycle either. I want to develop a plan of building generational wealth that will last for more than 3 generations and won’t cause the kids and grandkids to turn into spoiled trust fund brats. Here’s what I have come up with so far:

Building Generational Wealth Tool: The Dynasty Trust

When I began researching ways to grow and distribute wealth over long periods of time, the number one method I found was the Dynasty trust. Throughout most of U.S. History, and World History, trusts have been limited in time. Only since 1986 have perpetual trusts become an estate planning tool. Individual states have differing laws on how long trusts can last for and in the mid 1980’s many began repealing “the laws against perpetuities.” Several states allow trusts to last forever, while some have greatly lengthened their time frames which were normally under 100 years to several hundred years.

The Dynasty Trust

- Heirs may receive $10,000 upon reaching age 25, $25,000 upon reaching age 30, and $100,000 upon reaching age 40. The remainder of allocated funds will be paid out at age 55.

- Heirs may receive $1 for $1 matching distributions on contributions to retirement accounts up to $5,000 per year.

- Heirs may receive $10,000 for the birth or adoption of each child.

Overall the ability to dictate how the money is used is a pretty cool feature of a dynasty trust. The problem with allocating money this way is that far into the future it may not be practical, as laws and societal norms change.

Problems with Dynasty Trusts:

As someone who has done some genealogical research, I have learned that as time goes on and as generations continue, the number of individuals in those generations grows exponentially, while the genetic relationship to the grantor decreases 50% with each generation. As an example, if the Grantor has 2 children, and they each have 2 children and so on and so forth, and the average age between generations is 25 years, then 200 years into the trust we will be on Generation 9 with 256 people in that generation and most likely around 448 total heirs are living (3 generations total). Also, that 9th generation will only share 0.39% of genes with the Grantor.

As time goes on administering a trust to so many people will be extremely difficult and thus costly. There are exponentially more people trying to gain money from the trust, and there will be difficulties in determining who qualifies for the money. Also, even with a large starting sum and decades of compounding returns, having so many beneficiaries will either completely drain the trust or will make each distribution essentially worthless. (Your check from the trust fund for this year is 52 cents, enjoy!)

Because further generations are so far removed from the Grantor, I think it is probable they will have less reverence for the money as well. A gift from a living grandparent or parent means more. You can connect with that person, you can know their life story, and how they earned that money. When Anderson Cooper spoke about not having a trust fund from the Vanderbilt fortune (His great great great grandfather was Cornelius Vanderbilt) he said “My dad grew up really poor in Mississippi — I paid attention to that because I thought that’s a healthier thing to pay attention to than like some statue of a great great great grandfather who has no connection to my life.”

Taxes and changes in tax law are also a major caution with Dynasty trusts. Believe it or not, the tax laws in the United States change fairly often and from time to time there is a lot of anti-wealth sentiment in this country. I would not be surprised if in the futures vehicles such as Dynasty trusts are given extremely high tax rates, if not outright seized. For more on problems with Dynasty Trusts, check out this article. For all of these reasons I don’t think that dynasty trusts are the best way to go about building generational wealth.

My Plan For Building Generational Wealth:

Since I don’t believe that a Dynasty Trust is the best way to pass on wealth for all the reasons I outlined above, I want to do something more difficult, but that I think will be much more successful over the long term. I want to start a tradition of excellent money management and purposeful generational giving. Here is the basic framework for what I want to accomplish and how I will accomplish it. Also, check out my book “For My Children’s Children” on building generational wealth!

How To Build Generational Wealth Book

Building Generational Wealth For My Children:

I have 4 children in my life (1 step son, 1 biological son, and 2 nephews). These are the kids who live with me and that I am responsible for. I have 2 other nephews and a niece, but my financial responsibility to them is not the same. My kids are currently 13, 8, 5, and 3. When it comes to building generational wealth, obviously the most challenging is the 13 year old. He will become an adult before we reach financial independence, whereas the rest of the children will not.

1. Free room and board: I do not subscribe to the theory that our children need to be out the door at 18, nor do I believe that they should be living at home doing nothing but smoking weed and playing video games on my dime. My kids will be able to live at home for up to 5 years after graduating high school in the event that they are doing all of these things:

- 1. Going to further education: We have a community college 2 miles from our house that all of our kids have 100% scholarships to for 2 year associates degrees.

- 2. Working: They will be required to have jobs, or be self employed.

- 3. Saving money: They will be required to save a minimum of 50% of their income.

2. Retirement matching funds: Starting with their first paycheck We will match 50% of what they put into retirement funds for 5 years, up to $5,000 per year, for a total of $25,000 per kid. What this does is ensure that they get to $64,000 quickly, which is a major step in building a retirement nest egg, as outlined in my article Double Your Money.

3.Financial Guidance: I will also encourage my children to purchase a home as quickly as possible, with a 15 year or shorter fixed rate mortgage with a 20% down payment that costs less than 1 weeks paycheck. They may also receive 50% matching funds on a first home down payment, if we are in a position to do so.

4. Job Assistance: I think this is highly overlooked in our society. Helping people find the right job for them is key to getting ahead. I spent 3 years working for right around minimum wage because the employer worked around my school schedule. In retrospect I bet I could have found a job paying twice as much per hour had I looked diligently that I could have built my school schedule around. I will put in a lot of effort into helping my kids develop skills and find jobs that are higher paying, especially when starting out. The best way for this to succeed is for the kids themselves to be highly involved in building generational wealth.

Building Generational Wealth For My Grandchildren:

It’s crazy that I’m thinking about grandchildren, but historically speaking I could be only 5 years (or less) away from this. Yikes! My number one goal is to make sure that my kids delay becoming parents until they are stable in life and at least in their mid to late 20s. Being a teen parent is no fun and is a huge barrier to financial stability.

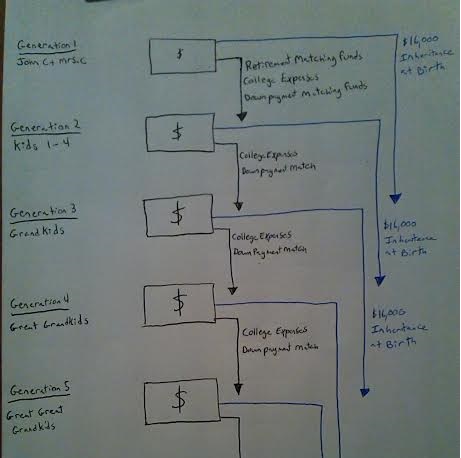

When my grandchildren are born I want to give them their inheritance. Each grandchild will receive the same amount of money, which will be $16,000. $8,000 from me, and $8,000 from Mrs. C. This money will be placed in a taxable brokerage account with their parents as the guardian until they are 18 years old. The money will be invested in a Mid-Cap Growth index fund, which gives off very little dividends so that while minors they should not have to file a tax return. Building generational wealth is much easier when you start at birth rather than starting in their 50s or 60s.

$16,000 at 8% annualized returns will be $60,000 at 18, $700,000 at 50, and $1 Million at age 55. Effectively I am funding their retirement. As I noted in my article Double Your Money, the goal is to reduce the amount of doubling periods needed. By giving them $16,000 we are eliminating 4 out of 10 doubling periods on the way to $1 million and gaining 2 doubling periods by starting at birth instead of at 20. By starting at birth we are also giving them a 50 – 60 year time horizon for needing the money. Hopefully we will not have any grandchildren until our oldest is 25 or older. This will allow us to be mostly done with matching funds to our children’s retirement accounts before we start funding this.

A rough sketch of how this will work…Sorry..my drawing and penmanship is atrocious.

But Wait, All These Capital Gains Are Taxable!!

Yes, they are, and we want to avoid paying tax as much as possible.

Currently long term capital gains are taxed at a 0% rate as long as the tax filer is in the 10% or 15% tax bracket. Currently this would be single filers with a taxable income of $37,950 or below. When adding in the standard deduction and 1 exemption, this results in an AGI of $48,350. For married filers the amounts are doubled.

There is also a “kiddie tax” on unearned income. Essentially, the first $1,000 of unearned income is tax free, the 2nd $1,000 is taxed at the dependent’s tax rate, and anything over $2,000 is taxed at the parents tax rate. Because of this we don’t want to harvest capital gains until the grandchild is either 25 or is able to claim himself as a non-dependent filer.

Most likely the children will become non-dependents at age 18 by earning enough money to provide for over half their own support. During these years it would make sense to harvest as many capital gains as possible by selling the assets in this account, up until they have emptied the account and repurchased new investments, now with a new cost basis equal to the total value in the account, rather than $16,000. Building generational wealth is much easier when you know the tax laws and take action to avoid overpaying on taxes.

As an example:

It reasonably costs around $12,000 per year to support a person. If at age 18 these kids work 1200 hours at $10 per hour they would hit this threshold. Now they can claim themselves as non-dependents.

Now, they can sell assets and take LTCGs of $36,350 per year. They should then immediately re-invest the proceeds into their own Roth IRA to the max, and into their own taxable account. After 2 years the account that I funded is empty.

Now at age 20 they have roughly $11K in a Roth IRA that will never be taxed and $65K in a taxable account with a tax basis of $65K. Since this is all “new money” now, it is much easier to deal with. They can either keep it in the taxable account, or as time goes on filter this money into their IRAs and 401Ks.

Building Generational Wealth: Continuing The Legacy:

For Our Children:

Since my kids are receiving a substantial amount of help with getting started in life and we are funding their kids’ retirement, by the time our grandchildren are grown, Our children will be in a position to also provide the same assistance we provided to our children, without having to provide retirement matching funds.

- Pay for college, preferably 2 years at a community college, and free room and board while living at home

- Requirements to work and save 50% of their income while living at home

- Matching funds for the down payment on a house in a modest home up to 50% of the cost of the median home in the country.

- Fund their grandchildren’s retirement funds with $16,000 (inflation adjusted from 2016 dollars).

For our Grandchildren:

Each grandchild will receive a book when they are 18. It will be a leather bound highly decorated book that will certainly stand out as something special. In it will be a collection of my articles covering virtually everything they could need to be successful in life. At the beginning of the book will be an introduction with something to the effect of:

“At your birth, your grandparents gifted you $16,000 in long term growth stocks. This money by now is most likely 4 times that amount. If you never add anything to it, by 65 you will have $2 million. They effectively prepaid your retirement. This money should not be spent on anything else. There will be no more gifts given for mishandling of these funds. You are also encouraged to continue saving at least 20% of your income and to join in the journey of building generational wealth.

Your parents are paying for your college and will provide matching funds for the down payment on your first house. When you have children they will also gift them $16,000 (inflation adjusted from 2016 dollars) in long term growth stocks.

It is expected that you will do the same for your children and grandchildren to keep our family from sinking into poverty. You have been given an amazing head start in the game of life, it is up to you to keep running the race and build on your family legacy.

Buy a home, raise children and pay for their education. Pay for your grandchild’s retirement, and pass this knowledge on to your children and grandchildren.”

What This System Gains Over A Dynasty Trust:

It keeps accounts from lasting for generations: The longer an individual account lasts, the more complicated it will become and the more likely it will be subject to taxes and possible seizure.

It keeps the giving in a tight family group. After my grandchildren I am not contributing any more money. Every gift of money comes from the parents or the grandparents. These are people who the heirs know and can relate to.

What this system lacks:

The one glaring problem with this system is that it hands over roughly $64,000 to an 18 year old. This can certainly be dangerous. If there is a problem with responsibility level this could be a bad thing. The only way to avoid this potential error would be to put the money in a trust fund administered by the parents, but that adds a lot of complexity. The best solution is to spend a lot of time and energy on raising responsible kids.

How Will I Afford This Plan of Building Generational Wealth?

Bam! That’s the big question right? That’s an awful lot of money we are talking about. The matching gifts for retirement savings will certainly be our biggest hurdle. For our oldest we will still be saving aggressively for our retirement when these matching funds start, but the majority of our nest egg will be complete and our house will be paid off. Essentially instead of saving around $45,000 per year at that point in time, we will be saving around $40,000 per year. This won’t affect our wealth building substantially.

The bottle neck comes when I am 43 and through age 47. During these years we will be providing matching funds for 2 kids and in 1 year we will be providing matching funds for 3. It is also highly probable during this time frame our oldest will start having kids, so that could be a large financial outlay during those few years. I am planning on working part time up until age 50 and with what our living expenses are and what my income level is now, the matching funds should not be a problem. In order to fund the grandchildren’s retirement I may have to work part time for an extra year or two to ensure I can do that, but it’s a small price to pay for building generational wealth to the degree we have planned.

End Of Life Gifts:

Although Dr. Aubrey Degrey strongly believes that the first human to live to be 1,000 has already been born, I have my doubts that I am that human. Eventually I will die, and when I do I think it is likely that Mrs. C. and I will have a net worth of several million dollars (…BTW that seems so freaking weird to say!) For the most part this money will go to charitable causes. Most likely to activities similar to the Bill and Melinda Gates Foundation and to The Carter Foundation, which work towards eradicating infectious diseases. Polio and Guinea worm will be eradicated very very soon, but there are still several diseases left to tackle. We may also contribute some money to preserve land in our area as forests and to build nature trails. I don’t plan on any individuals or family members receiving a large sum of money upon our deaths. There very well may be a large sum of money, but it won’t be an inheritance. So long as we live average lifespans we will have finished our part in building generational wealth decades before we pass.

The Path Forward To Building Generational Wealth:

I am going to essentially ensure that my children and grandchildren will start off adult life with at least $64,000 in retirement savings, which will provide for a modest retirement without adding any more money to it (Although they still should add some). Each generation thereafter will be responsible for paying for the retirement of their grandchildren. Since they don’t need to save for their own retirement and had further education covered as well, it should not be a strain to put $16K – $32K into each grandchild’s name at birth.

I know that this plan isn’t fool proof, and it is possible along the way someone may break the chain of giving. I think this is the best framework I can develop, but over time I may make some more adjustments to it in order to increase the likelihood that this income and wealth is used effectively.

Have you thought about a plan for giving inheritances? Do you think it is better to give inheritances while living or posthumously? What do you think is a good method to go about building generational wealth?

Leave a Reply